Investing can be one of the most rewarding ways to build long-term wealth, but for beginners, it can also be confusing and intimidating. The truth is that most new investors don’t lose money because the markets are unpredictable, they lose money because of easily avoidable mistakes. Whether you’re just starting your investment journey or have been dabbling for a while, understanding these pitfalls can save you thousands (or even tens of thousands) over time.

In this comprehensive guide, we’ll break down the five most common investing mistakes, explain why they happen, and show you exactly how to avoid them. You’ll also get actionable steps, real-world examples, and expert-backed tips to help you invest smarter and grow your wealth consistently.

1. Trying to Time the Market

Perhaps the most common and most costly investing mistake beginners make is trying to “time the market.” This means attempting to predict when prices will go up or down, buying just before a rally, and selling just before a crash. It sounds logical in theory, but in practice, even professionals struggle to do it successfully and consistently.

Why Market Timing Doesn’t Work

Research from https://www.morningstar.com/articles shows that over 90% of investors who try to time the market end up earning less than those who simply stay invested. Market timing often leads to two dangerous behaviors:

- Panic selling: Selling investments when prices drop, locking in losses that could have recovered with time.

- FOMO buying: Buying at market highs out of fear of missing out, only to watch prices drop afterward.

Instead of trying to outsmart the market, focus on time in the market staying invested for the long haul. The longer your money remains invested, the greater your chances of benefiting from compound growth.

Example of the Power of Staying Invested

Imagine two investors:

- Investor A invests $5,000 per year consistently, no matter what happens in the market.

- Investor B tries to time the market and misses the 10 best days each year.

After 20 years, Investor A could easily have tens of thousands more simply because they stayed invested through the ups and downs. Missing just a handful of the best-performing days can dramatically reduce your returns.

Practical Tip

Use a dollar-cost averaging (DCA) strategy: invest a fixed amount regularly (for example, every month), regardless of market conditions. This approach reduces emotional decision-making and averages out your cost over time.

2. Not Diversifying Enough

“Don’t put all your eggs in one basket.” You’ve probably heard this saying and it applies perfectly to investing. Many beginners make the mistake of putting all their money into a single stock or sector, like tech or crypto. When that area takes a hit, their entire portfolio suffers.

What Diversification Really Means

Diversification means spreading your investments across different types of assets, sectors, and even geographic regions. This helps reduce overall risk and increase stability. A well-diversified portfolio might include:

- Stocks: Large-cap, mid-cap, and small-cap companies.

- Bonds: Government or corporate bonds to balance volatility.

- ETFs or Index Funds: Affordable, diversified funds tracking entire markets.

- Alternative assets: Real estate, REITs, or even commodities like gold.

Case Study of the 2020 Market Crash

During the 2020 pandemic crash, investors heavily concentrated in airline and hospitality stocks saw massive losses of over 50%. Meanwhile, diversified investors with exposure to healthcare, tech, and bonds saw smaller declines and recovered faster.

Beginner Tip

Start with a diversified index fund or ETF, such as the S&P 500 or Total Market Index Fund. These funds give you instant exposure to hundreds of companies, spreading your risk automatically.

Common Mistake to Avoid

Avoid “false diversification” , owning multiple funds that actually hold the same stocks. Always check the fund composition before investing.

3. Ignoring Fees and Hidden Costs

Fees might seem small at first glance, such as a 1% management fee or a few dollars per trade. But over time, these charges can eat away a significant portion of your returns. Many beginners overlook how powerful compounding costs can be.

The Hidden Impact of Fees

Let’s say you invest $10,000 at a 7% annual return for 30 years. With a 1% fee, your ending balance would be around $574,000. Without that fee, it would be $761,000. That is a difference of nearly $187,000. That is the price of ignoring fees.

How to Keep Costs Low

- Choose low-cost index funds or ETFs with expense ratios under 0.2%.

- Avoid frequent trading every transaction may trigger fees or taxes.

- Compare platforms: Some brokers charge 0% commission on trades.

- Be cautious of actively managed funds with high management fees and low outperformance.

Beginner Mistake: Chasing High Returns

Many new investors fall for flashy funds or “exclusive” investment products promising high returns, often with high fees. In reality, very few active funds outperform low-cost index funds over the long term.

Remember: In investing, you control what you pay, not what you earn. Keeping costs low gives you a guaranteed edge.

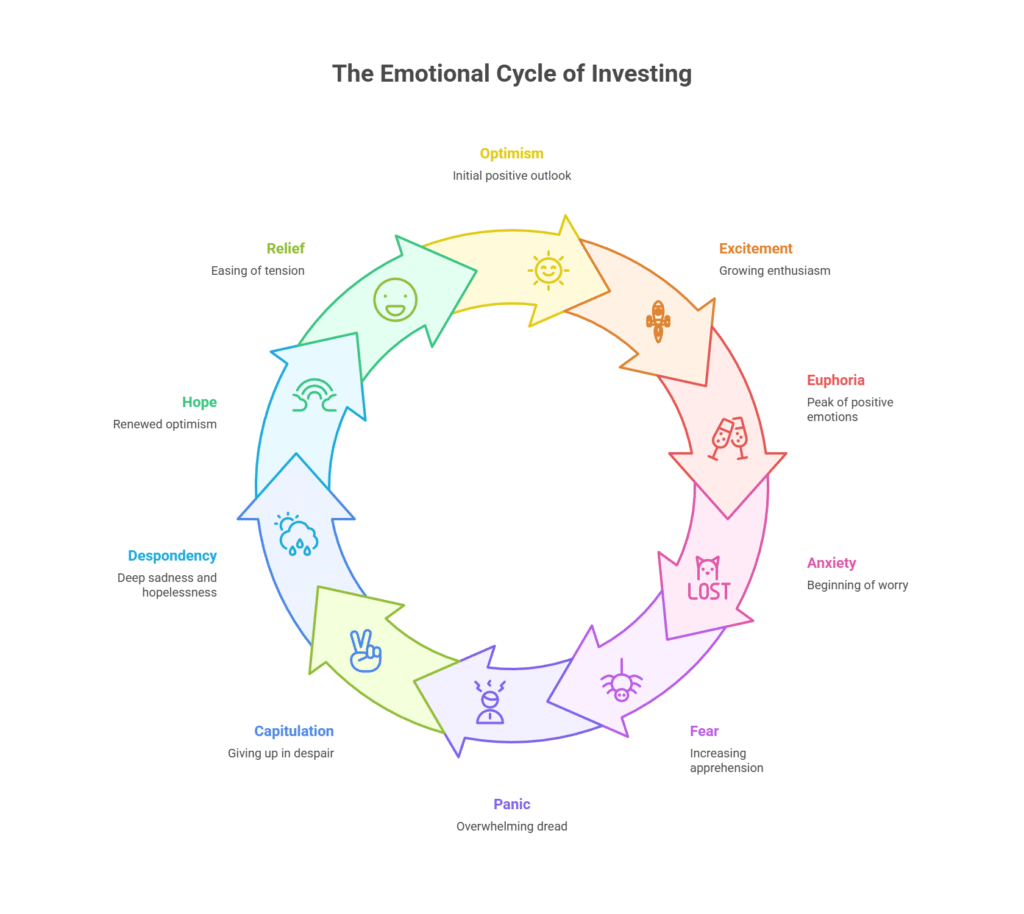

4. Letting Emotions Drive Decisions

Emotions are powerful and dangerous when it comes to money. Fear, greed, and impatience are the biggest enemies of long-term investing success. Market volatility can trigger emotional reactions that lead to bad decisions.

The Emotional Investing Cycle

When markets rise, greed takes over. Investors rush in, convinced the good times will last forever. When markets fall, fear takes hold and panic selling begins. This constant cycle leads to buying high and selling low, the exact opposite of what successful investors do.

How to Manage Emotions When Investing

- Have a plan: Set predefined rules for buying, selling, and rebalancing your portfolio.

- Stay informed: Follow credible financial news from https://www.investopedia.com/ or https://www.cnbc.com/.

- Don’t check your portfolio daily: Obsessive monitoring fuels emotional decision-making.

- Practice mindfulness: Recognize emotional triggers and remind yourself that volatility is normal.

Expert Insight

Warren Buffett famously said, “Be fearful when others are greedy and greedy when others are fearful.” Successful investing requires discipline, patience, and emotional detachment.

Pro Tip

Automate your investments through robo-advisors or recurring transfers. Automation removes emotion from the process and ensures consistent investing habits.

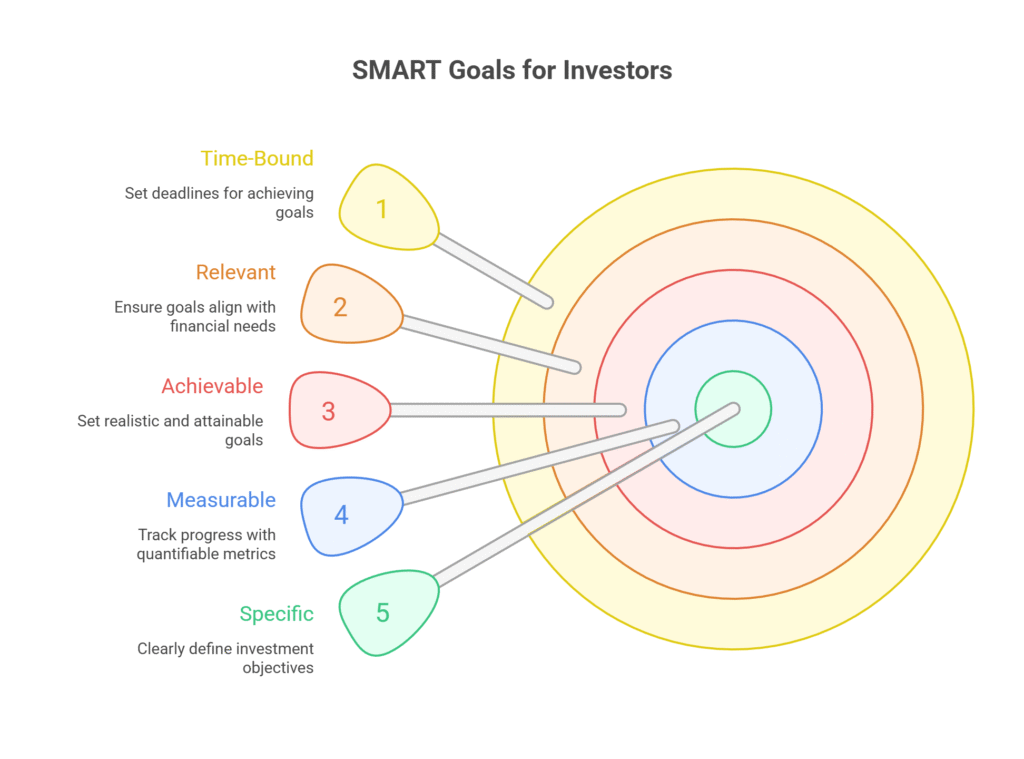

5. Not Having Clear Financial Goals

Investing without clear goals is like driving without a destination. You might be moving, but you don’t know where you’re going. Every investment decision should align with a specific goal, such as buying a home, retiring comfortably, or achieving financial independence.

Why Goals Matter

Your financial goals determine your time horizon, risk tolerance, and investment strategy. For example:

- Short-term goals (1–3 years): Low-risk investments like high-yield savings or bonds.

- Medium-term goals (3–10 years): Balanced portfolios with stocks and bonds.

- Long-term goals (10+ years): Growth-focused portfolios with stocks.

Step-by-Step Guide to Setting Clear Investment Goals

- Define what you’re investing for (specific, measurable goal).

- Determine how much money you’ll need and by when.

- Decide how much you can invest each month.

- Choose appropriate investment vehicles.

- Review progress yearly and adjust as needed.

Beginner Tip

Use goal-setting tools to visualize and track your investment milestones. These tools help align your investments with your life priorities and reduce decision fatigue.

Bonus Tip: Start Small but Stay Consistent

Many new investors believe they need large amounts of money to start, but that is a myth. Thanks to modern platforms and fractional shares, you can start investing with as little as $10.

The Magic of Compound Growth

Compounding means earning returns on your previous returns. It creates a snowball effect that grows faster over time. Albert Einstein famously called it “the eighth wonder of the world.”

For example, investing just $100 per month at a 7% average return will grow to over $120,000 in 30 years. The earlier you start, the more compounding works in your favor.

Action Plan for Beginners

- Start with small, regular investments — even $25 per week matters.

- Automate deposits to your investment account.

- Reinvest dividends to maximize compounding.

- Stay invested — time, not timing, builds wealth.

Common Mistake to Avoid

Waiting for the “perfect moment” to start. The best time to begin investing was yesterday. The second-best time is today.

Final Thoughts

Every successful investor was once a beginner. Investing mistakes are part of the learning process, but by understanding and avoiding the common pitfalls outlined here, you’ll dramatically improve your odds of success.

Successful investing is about consistency, patience, and education. Focus on long-term goals, diversify wisely, keep fees low, and manage your emotions. The sooner you build these habits, the sooner your money starts working for you.

Take Action Today: Review your portfolio, automate your contributions, and set clear goals for your future. The sooner you begin, the greater your financial freedom will be tomorrow.

Frequently Asked Questions

1. How much should I start investing with?

You can start investing with as little as $10–$50. The key is consistency — small, regular investments compound over time and grow faster than you might expect.

2. What’s the safest way for beginners to start investing?

Begin with diversified, low-cost index funds or ETFs. They provide exposure to hundreds of companies, spreading risk while offering steady long-term returns.

3. Should I pay off debt before investing?

Focus first on paying off high-interest debt (like credit cards), but you can still invest small amounts to build the habit. Once debt is under control, increase your contributions.

4. How often should I check my investments?

Once per month is enough for most investors. Constantly checking your portfolio can lead to emotional decisions and unnecessary stress.

5. What are the best investing platforms for beginners?

Consider user-friendly platforms, which offer educational tools, automatic investing, and low or zero fees.