For many growing businesses, access to capital is the difference between momentum and stagnation. Whether you’re a startup scaling quickly or an established company targeting new markets, the right funding model can fuel expansion, improve cash flow, and help you hire new talent. But when searching for new capital, founders often face two primary options, revenue-based financing and traditional debt financing. Understanding how each works, and which aligns best with your business model, can help you avoid costly mistakes while maximizing growth outcomes.

This guide explores both financing options in detail, compares them side-by-side, explains when to choose each, and highlights alternative capital sources like private money lending and even investment property loans (for real estate-backed businesses). We’ll also explain how a financial broker fits into the process and how to evaluate terms, risks, and repayment obligations thoughtfully. If you’re trying to determine which option is better for your business, this guide has everything you need.

Understand How Revenue-Based Financing and Traditional Debt Work

Before you can compare revenue-based financing (RBF) and traditional debt, it’s critical to understand their core mechanics. These funding models are built on different philosophies, each affecting your company’s cash flow, operational flexibility, and long-term cost of capital.

What Is Revenue-Based Financing?

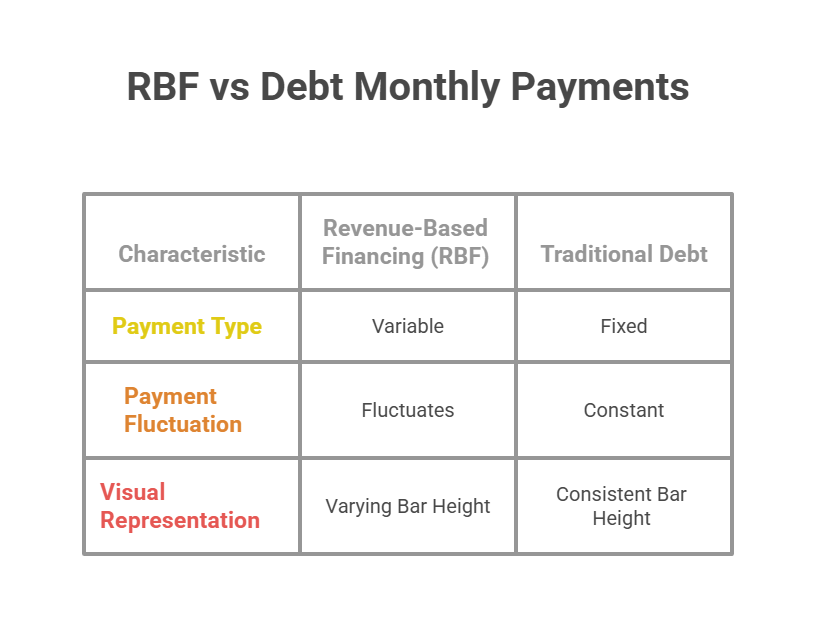

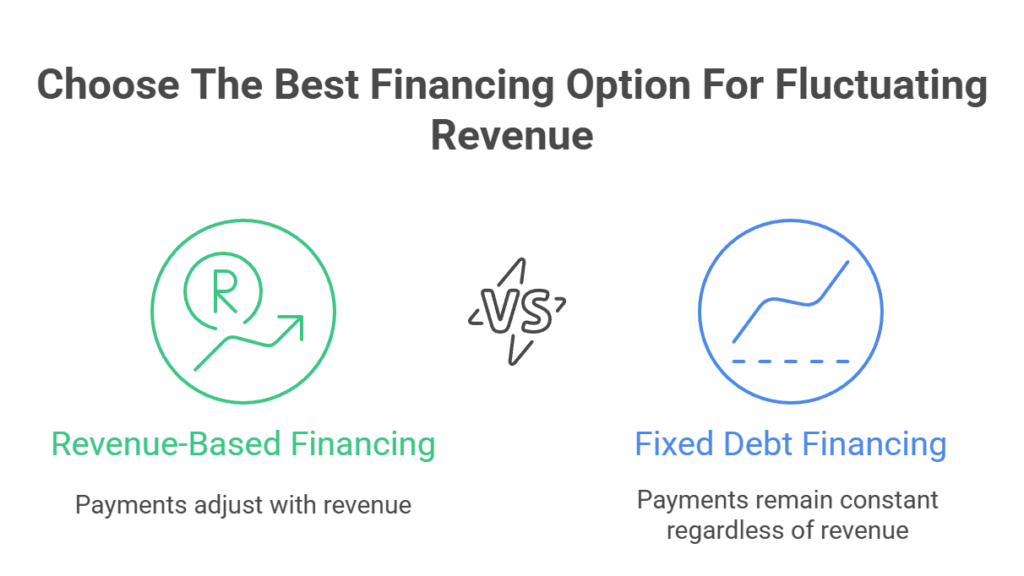

Revenue-based financing allows businesses to receive upfront capital in exchange for repaying a percentage of future monthly revenue until a predetermined repayment cap (like 1.3x to 1.8x the funded amount) is reached. Unlike loans with fixed monthly payments, RBF adjusts with your revenue. If you have a slow month, you repay less. If revenue accelerates, you repay more quickly.

RBF is often favored by subscription-based businesses, eCommerce brands, and SaaS companies with high gross margins and predictable revenue. Investors, sometimes called RBF providers, focus on top-line revenue rather than traditional collateral. This makes approval faster and more flexible, especially if traditional lenders won’t work with you.

Example: A DTC brand receives €200,000 with a 1.5x payback cap. Each month, they remit 6% of revenue until they repay €300,000 total. Slow months mean lighter payments. Strong months accelerate repayment.

What Is Traditional Debt Financing?

Debt financing is the most familiar funding model. You borrow money and repay it on a fixed schedule over time, usually with interest. This includes everything from credit lines and business loans to financing options secured by assets. Traditional lenders evaluate creditworthiness, cash flow, and collateral before approving a loan.

Loans often involve fixed payments, common for term loans, or variable payments tied to interest rate shifts. Decision timelines can be slower because lenders evaluate risk and may require personal guarantees. Still, debt financing typically offers a lower cost of capital compared to RBF if you qualify.

Example: A business secures a €200,000 loan at 9% interest over five years. They make predictable monthly payments regardless of revenue fluctuations.

How Private Money Lending Fits Into the Financing Landscape

An adjacent option is private money lending, usually offered by individuals or private groups rather than banks. These short-term loans often carry higher rates than institutional loans, but can be faster, more flexible, and secured by specific assets. Real estate investors commonly use private money lending or investment property loans to fund acquisitions.

In business contexts, private lenders may require collateral or steep interest if credit is weak. When evaluating private money lending, a financial broker can connect you to vetted lenders and help negotiate terms. While strong RPM opportunities exist here, this option should be weighed carefully due to risks.

Key Differences Between RBF and Traditional Debt Financing

Revenue-based financing and debt financing serve similar goals, injecting capital into the business, but they differ significantly in structure and cost. Selecting the right one depends on your business model, financial strength, and risk appetite.

1. Repayment Flexibility

RBF aligns your repayment schedule with revenue performance. If revenue dips, payment dips, making it an appealing option for seasonal businesses or early-stage companies lacking predictable cash flow. In contrast, debt financing demands fixed payments, irrespective of fluctuations, making cash flow management crucial. Missing payments may trigger penalties or credit damage.

For businesses without predictable income, RBF’s flexibility may protect operating liquidity. On the other hand, predictable fixed payments can be easier to plan for, and loan amortization can provide clearer financial projections.

2. Cost of Capital

The total payback on RBF can be significantly higher than traditional debt. While bank loans might charge 7–13% annual interest, RBF caps often equate to effective APRs of 20–40%+ depending on speed of repayment. Faster growth means faster, and therefore more expensive, RBF repayment.

In contrast, traditional debt offers lower cost but requires stronger credentials. If you qualify, it’s typically the more cost-efficient solution long-term. However, if you don’t qualify, RBF may be your next best option, even at a higher price.

3. Risk and Collateral

Traditional debt may require collateral, personal guarantees, or both. If a business defaults, lenders may seize pledged assets. RBF doesn’t typically require collateral or PGs, reducing founder personal risk. However, investors often examine gross margin quality before funding.

Where collateral exists, such as with investment property loans, the lender’s risk decreases, which can lead to better terms.

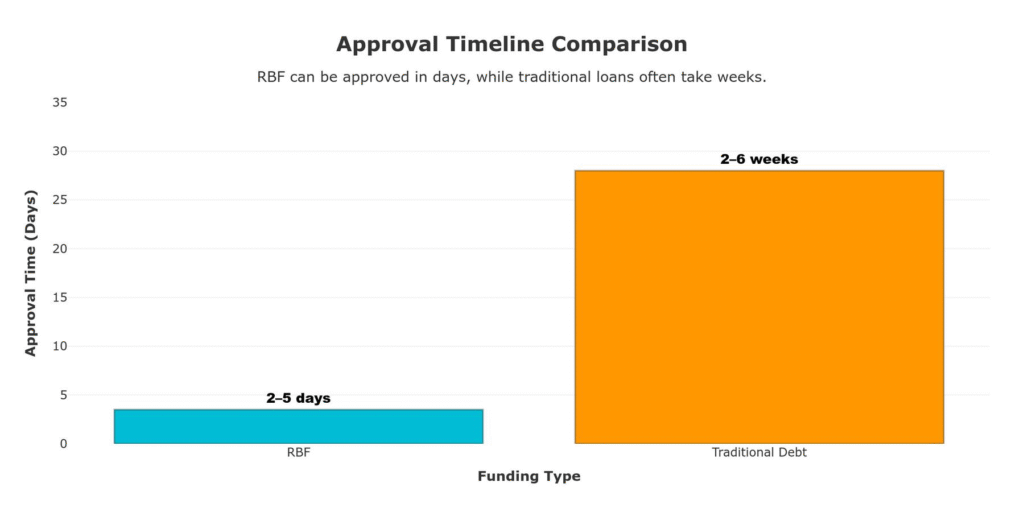

4. Approval & Speed

RBF underwriting is primarily revenue-driven. Providers may approve funding in days, not weeks. Traditional lenders may request financials, tax returns, and asset appraisals, typically lengthening the process.

A financial broker can speed up underwriting by helping match borrowers with lenders who fit their profile.

5. Use Cases

RBF funding works well for businesses with:

- Predictable monthly revenue

- High gross margins

- Limited hard assets

- Seasonal patterns

Traditional debt financing is more suitable when:

- You have steady financials

- You want lower costs

- You can provide collateral

- You prefer predictable payments

Explore the Pros and Cons of Revenue-Based Financing

Revenue-based financing has gained popularity because it offers fast, founder-friendly capital. But it’s not always the cheapest or best fit. Let’s examine its major advantages, drawbacks, and ideal scenarios.

Major Advantages

- No collateral or personal guarantees.

- Payments scale with revenue.

- Fast approval.

- Non-dilutive.

- Flexible use of funds.

Potential Drawbacks

- Higher cost of capital.

- Fast repayment increases effective APR.

- Not suitable for low-margin businesses.

- Limited availability in some regions.

Ideal Use Cases

- SaaS startups with consistent MRR.

- DTC or eCommerce brands with recurring revenue.

- Seasonal businesses.

- Businesses that cannot or will not provide personal guarantees.

Understand the Pros, Cons, and Scenarios for Traditional Debt Financing

Traditional debt financing has been the backbone of business expansion for generations.

Major Advantages

- Lower cost long-term: Bank interest rates beat most alternative financing models.

- Predictable payments: Easier financial planning.

- Wide availability: Accessible via banks, online lenders, and government programs.

- Larger loan amounts: Suitable for major expansions.

Drawbacks

- Credit and collateral required

- Longer approval timelines

- Personal guarantees common

- Fixed payments stress cash flow

These trade-offs are particularly visible in asset-backed lending. For example, a company taking investment property loans often receives more favorable terms because lenders secure collateral. Meanwhile, companies using unsecured term loans might face higher requirements.

Best Use Cases

- Established companies with strong credit

- Companies acquiring assets

- Businesses expanding or opening new locations

- Businesses requiring cheaper capital

- How Private Money Lending and Financial Brokers Fit In

How Private Money Lending and Financial Brokers Support Borrowers

Private money lending differs from both RBF and traditional debt financing. Private lenders, individuals or small firms, offer short-term loans, often at higher rates. These loans can be approved quickly and are sometimes collateral-backed (especially in real estate projects).

In some industries, founders work with a financial broker to match with suitable lenders (traditional or private). Brokers help gather documentation, negotiate terms, and present deals to lenders with higher success rates.

Private Money Lending Advantages

- Fast approvals

- Flexible underwriting

- Asset-backed borrowing

Drawbacks

- Higher rates

- Short terms

- Foreclosure risk if asset-backed

Side-by-Side Comparison of RBF and Traditional Debt

Use this comparison table to visualize the best option for your business:

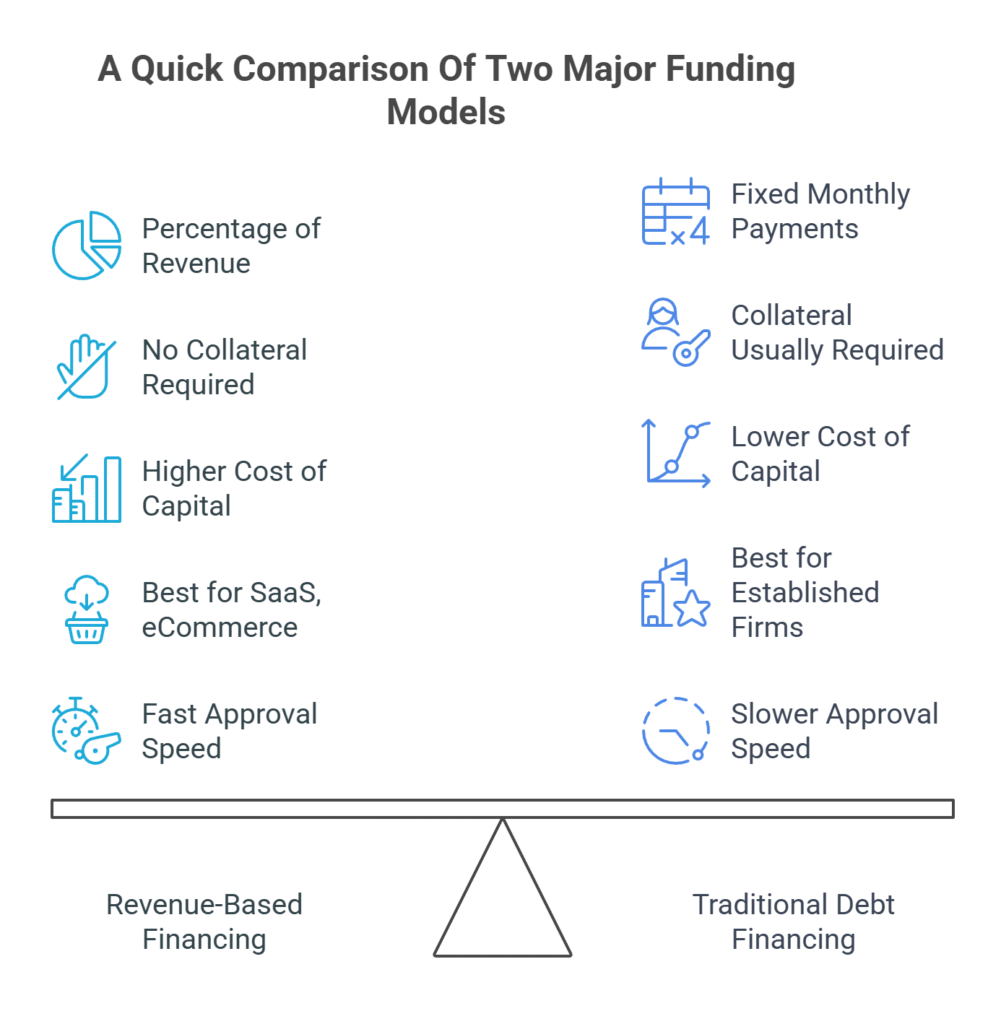

| Feature | Revenue-Based Financing | Traditional Debt Financing |

|---|---|---|

| Payment structure | % of revenue | Fixed monthly payments |

| Collateral/PG | No | Usually |

| Cost of capital | Higher | Lower |

| Best for | SaaS, eCom | Established firms |

| Approval speed | Fast | Slower |

How to Choose the Best Financing Option for Your Business

Neither model is universally “better.” The right choice depends on revenue volatility, financing urgency, collateral availability, and long-term cost sensitivity.

Choose Revenue-Based Financing If:

- You have recurring or predictable revenue

- You need fast capital

- You don’t want personal guarantees

- You run a seasonal business

Choose Traditional Debt If:

- You can qualify based on credit and collateral

- You want the lowest cost

- You prefer fixed payments

- You plan long-term capital allocation

Frequently Asked Questions

1) Is revenue-based financing cheaper than debt financing?

Usually no. RBF is typically more expensive because of higher risk and flexibility. Traditional debt often has lower interest costs.

2) Do I need collateral for revenue-based financing?

No. RBF typically doesn’t require collateral or personal guarantees; approval is revenue-based.

3) Is private money lending risky?

It can be. Rates are higher and terms shorter. If loans are asset-backed, lenders can seize the collateral.

4) Are investment property loans only for real estate?

Yes. These are specifically asset-backed loans used to purchase or refinance investment real estate.

5) Should I work with a financial broker?

Working with a financial broker can simplify the process, especially when evaluating multiple lenders.

Which Financing Option Should You Choose?

If your business is growing but revenue is inconsistent, revenue-based financing may be your best bet. It offers fast access to capital and flexible repayment. On the other hand, if you have steady financials and collateral, traditional debt financing offers a lower cost and predictable monthly payments. Private money lending offers speed and flexibility at a price, and working with a financial broker can help you navigate all options.

Take the next step by comparing offers from multiple lenders, evaluating your payback capacity using revenue projections, and consulting financial experts before signing any agreement.