Retirement planning is one of the most important financial decisions you can make, yet it is often overlooked, especially by young professionals. The earlier you start, the greater the advantage of compound interest, tax-advantaged accounts, and strategic investments. By taking consistent, informed action today, you can ensure a secure and comfortable retirement decades down the line.

This comprehensive guide will walk you through actionable strategies, investment options, budgeting tips, and common mistakes to avoid. Plus, it includes recommended tools and calculators to make your planning both practical and results-driven.

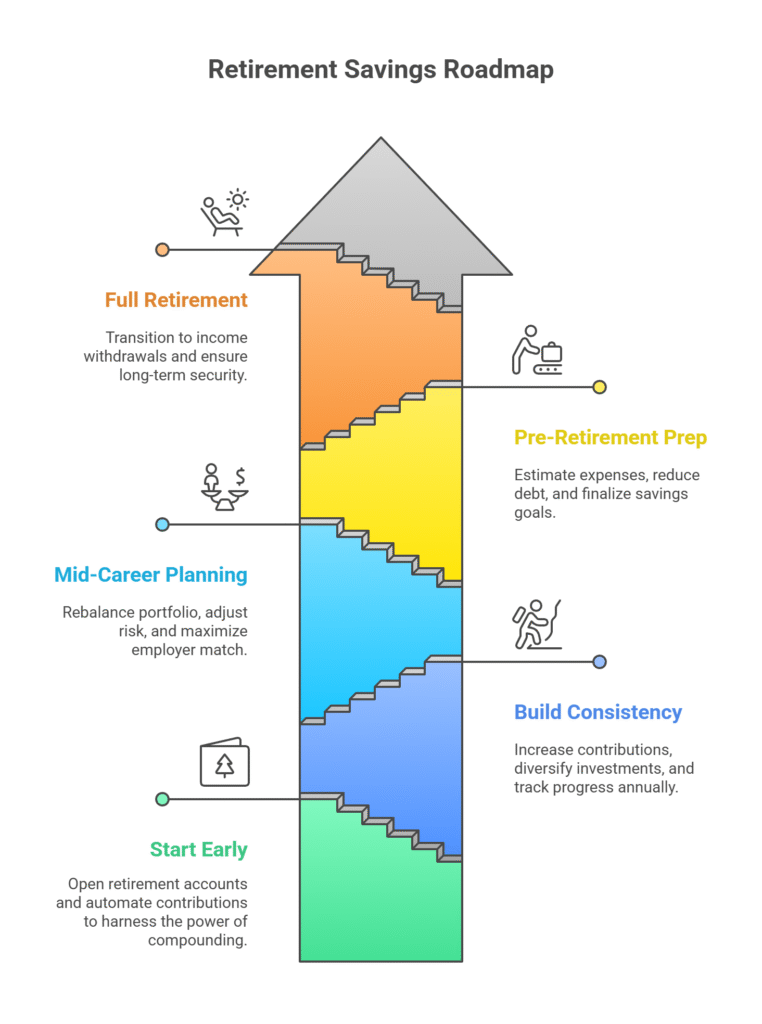

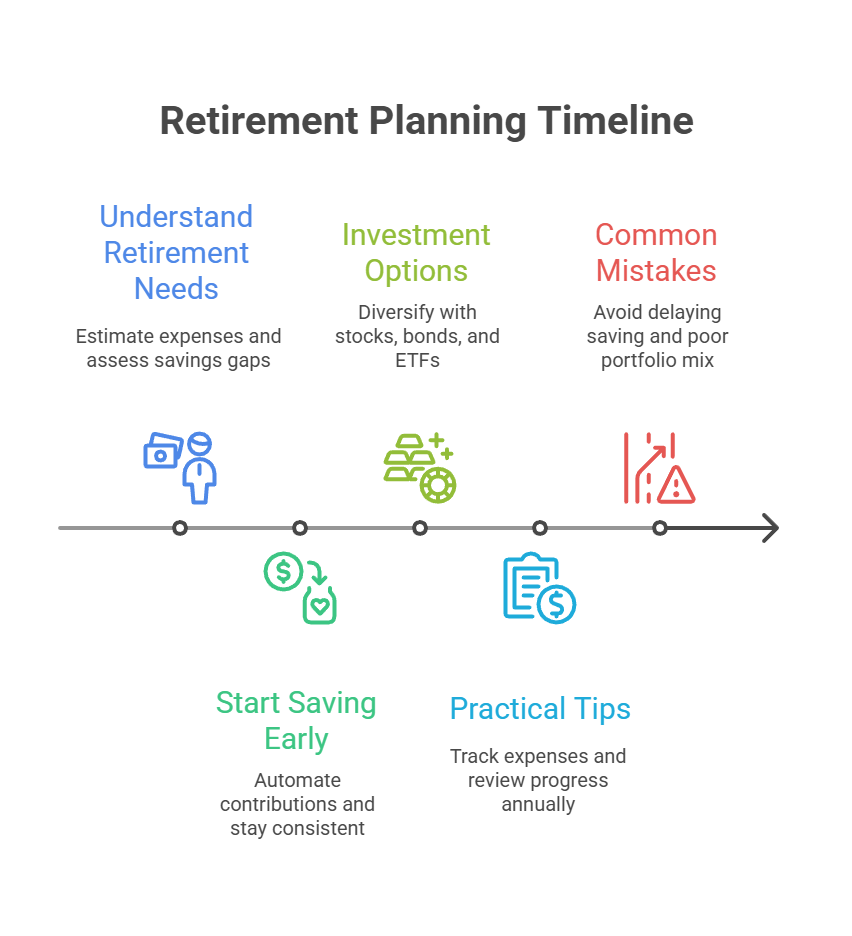

Step 1: Understand Your Retirement Needs

Knowing how much you need to retire is the foundation of a smart financial plan. Your retirement needs depend on your lifestyle goals, healthcare expectations, and projected living costs.

Estimate Living Expenses

Start by creating a detailed estimate of your monthly expenses in retirement:

- Housing: Mortgage-free living, rent, property taxes, or downsizing options.

- Healthcare: Medicare, insurance premiums, prescription costs, and potential emergencies.

- Daily Living: Food, utilities, transportation, and personal care.

- Leisure: Travel, hobbies, entertainment, and dining out.

Tip: Use a https://www.empower.com/tools/retirement-planner to model different lifestyle scenarios: conservative, moderate, or luxurious to determine realistic savings goals.

Factor in Inflation and Longevity

Inflation reduces purchasing power over time. Plan for an average annual inflation rate of 2–3%. Additionally, longevity is increasing, meaning your retirement savings might need to last 25–35 years or more. Incorporating these variables ensures your plan is robust and sustainable.

Assess Current Savings and Identify Gaps

Inventory your current retirement accounts, employer contributions, and personal savings. Compare them against projected needs to spot gaps. Early identification lets you adjust your savings strategy accordingly.

Tip: Track your progress using a retirement calculator. This helps visualize your current trajectory and necessary adjustments.

Step 2: Start Saving Early

The most critical factor in retirement planning is time. Compound interest magnifies your contributions over decades, making early action more impactful than large sums contributed later.

Harness the Power of Compound Interest

Example: Jane starts saving $200 per month at age 25, while Mark starts at 35. Assuming a 7% annual return, Jane ends up with over $260,000 more than Mark by age 65, despite contributing the same amount monthly. Small, consistent contributions early on can have a massive impact over time.

Automate Your Savings

Set up automatic contributions to your retirement accounts:

- 401(k) through your employer

- Traditional or Roth IRA ([affiliate:RothIRAProvider])

- Brokerage or investment accounts ([affiliate:InvestingPlatform])

Automation reduces the temptation to spend and ensures consistent growth over time. Gradually increase contributions as your income rises.

Start Small, Think Big

Even modest savings can grow into substantial amounts thanks to compounding. Prioritize consistency over large one-time deposits. Combine early savings with smart investments to maximize long-term growth.

Investment Options for Retirement

Diversifying your retirement portfolio balances risk and return while taking advantage of different growth opportunities. Consider a mix that aligns with your risk tolerance and retirement timeline.

401(k) and Employer-Sponsored Plans

401(k) plans are one of the most effective retirement vehicles, offering tax advantages and employer matching contributions:

- Contribute enough to receive full employer match this is free money.

- Choose investments based on your age: higher equity allocation when young, gradually shifting to bonds and stable assets as you approach retirement.

- Opt for low-cost index funds to reduce fees and maximize compounding.

Case Study: Sarah contributed 5% of her salary starting at 27 and gradually increased to 15%. With employer matching, she accumulated over $500,000 by 60, highlighting the benefit of early consistent contributions.

Individual Retirement Accounts (IRAs)

IRAs offer additional flexibility and tax advantages:

- Traditional IRA: Reduces taxable income now; taxes are due at withdrawal.

- Roth IRA ([affiliate:RothIRAProvider]): Contributions are post-tax, but withdrawals are tax-free in retirement.

IRAs also allow access to a wide range of investments, including stocks, ETFs, and mutual funds. Evaluate your current and future tax brackets to determine which IRA type suits your goals best.

Stocks, Bonds, and ETFs

Diversification across asset classes helps mitigate risk:

- Stocks: High growth potential, but higher volatility.

- Bonds: Lower risk, stable income streams.

- ETFs: A mix of multiple assets for balanced risk and growth.

Strategy Tip: Younger investors can prioritize equities for growth. As retirement nears, shift to bonds and stable ETFs to preserve capital.

Practical Tips to Maximize Retirement Savings

Automate Contributions

Automated transfers ensure regular contributions and reduce stress. Many platforms offer auto-increase features that increment contributions annually, helping you save more without thinking about it.

Track and Control Expenses

Budgeting apps can help identify discretionary spending. Reducing non-essential expenses frees up money to increase retirement contributions. Even small adjustments like reducing subscription services or dining out less can lead to significant long-term gains.

Review and Adjust Annually

Regular reviews help keep your plan aligned with life changes:

- Increase contributions with salary raises or bonuses.

- Rebalance your portfolio based on risk tolerance and market performance.

- Adjust retirement goals due to family changes, healthcare needs, or lifestyle aspirations.

Using a https://ownyourfuture.vanguard.com/content/en/learn/library.html can make these reviews more structured and actionable.

Common Retirement Planning Mistakes

- Delaying saving early action is critical

- Neglecting employer match opportunities

- Overly conservative or risky investments

- Ignoring inflation when planning withdrawals

- Failing to track and adjust your portfolio regularly

Avoiding these mistakes increases the likelihood of achieving your retirement goals without financial stress.

Frequently Asked Questions

1) At what age should I start saving for retirement?

Start as early as possible, ideally in your 20s. Early contributions benefit from compound interest, creating wealth even with smaller monthly investments.

2) How much should I save each month?

Target at least 15% of your monthly income if feasible. Adjust based on personal goals, age, and current savings. Automation and incremental increases make this more manageable.

3) What if I start saving late?

Don’t panic. Maximize contributions to retirement accounts, consider high-growth investments, and extend your working years if possible. Catch-up contributions in 401(k)s and IRAs are also available for those over 50.

4) Which is better: 401(k) or IRA?

Use both if possible. Employer 401(k)s offer matching contributions, while IRAs provide additional tax benefits and investment flexibility. Choosing depends on your income, tax situation, and desired investment options.

5) How can I protect my retirement from market volatility?

Diversify across stocks, bonds, and ETFs. Rebalance your portfolio annually. Avoid making emotional investment decisions during market swings, and gradually shift toward more stable assets as you near retirement.

Takeaways

Retirement planning is a long-term process that rewards consistency, strategy, and early action. Start by assessing your needs, automating savings, leveraging employer plans, and diversifying your investments. Use calculators, budgeting apps, and expert advice to make informed decisions and track progress.

Actionable Tip: Start today by setting up automated contributions to your retirement accounts. Even a small amount invested consistently can grow into a substantial nest egg over time. Combine early savings, diversified investments, and annual plan reviews to achieve a secure, comfortable retirement.