When you’re juggling one or more loans, the whole financial picture can feel heavy. The good news is that getting out of debt faster is less about dramatic sacrifices and more about a reliable system that blends math, psychology, and momentum. With a clear plan, a few tactical moves, and steady habits, you can shorten your payoff timeline, save substantial interest, and protect your mental energy in the process. This long-form guide walks you through everything, how to map your debts, pick a winning payoff method, free up cash without feeling deprived, reduce interest ethically, negotiate with lenders, and build a realistic schedule you can actually maintain.

Throughout the article you’ll find mini-case studies, simple formulas, practical checklists, and beginner tips you can act on today. Whether you’re paying off student loans, personal loans, a car note, or high-interest credit cards, these strategies will help you accelerate loan payoff responsibly, without burnout.

Get Total Clarity by Knowing Exactly What You Owe

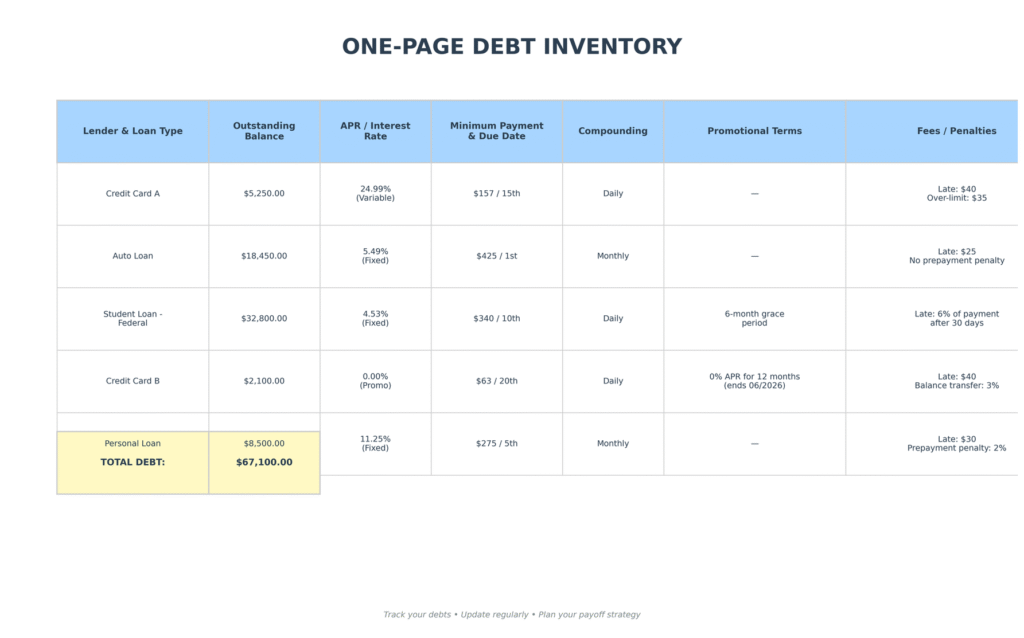

Debt payoff begins with an honest inventory. Many borrowers send automatic payments each month without seeing how much goes to interest versus principal. That lack of visibility quietly slows progress. Your first step is to build a single, accurate snapshot of every obligation so you can prioritize with intention.

Build a One-Page Debt Inventory

Open a fresh spreadsheet or note and list for each loan:

- Lender & loan type: e.g., “Credit card A,” “Auto loan,” “Student loan (fixed).”

- Outstanding balance: The amount you still owe today.

- APR / interest rate: Annual percentage rate, fixed or variable.

- Minimum payment & due date: Monthly obligation and calendar deadline.

- Compounding: Daily, monthly, or simple interest (if known).

- Promotional terms: 0% intro APR, teaser rates, or grace periods.

- Fees/penalties: Late fees, balance transfer fees, prepayment penalties, etc.

Seeing it all on one page turns a foggy problem into a solvable one. This inventory becomes your command center. You’ll update it monthly as balances fall and strategies change.

Why Clarity Saves Money

Interest accrues on balances, not intentions. Without precise numbers, it’s easy to underestimate how much interest you’re paying or misplace extra cash on loans that don’t move the needle. With clarity, you can target debts surgically, minimize interest, and avoid missed payments that harm your credit score.

Tip for beginners: if finding exact APRs or balances feels daunting, pull the latest statements or log in to each lender’s dashboard. You’ll have all the data within 20 minutes. Save those PDFs in one folder for quick reference.

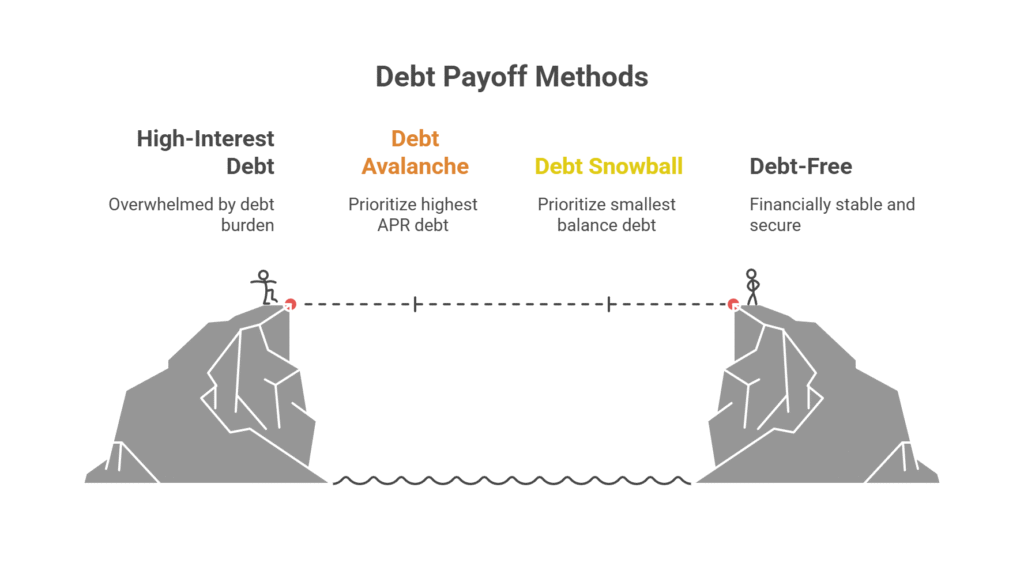

Choose a Payoff Engine by Comparing the Debt Avalanche and the Debt Snowball

Two proven methods dominate: the debt avalanche (mathematically optimal interest savings) and the debt snowball (psychology-first momentum). Neither is “right” for everyone; the best method is the one you will actually follow for months on end. Here’s how they work and how to choose.

Debt Avalanche (Math-First)

With the avalanche, you pay minimums on all loans and throw every extra euro at the highest interest rate balance first. Once that’s gone, you roll the freed-up payment into the next-highest APR, and so on. Because you attack the costliest interest first, you pay less over time and often finish faster overall.

Mini-example: Suppose you owe:

- Credit Card A: €2,200 @ 25% APR, €60 minimum

- Credit Card B: €1,400 @ 21% APR, €45 minimum

- Auto Loan: €6,800 @ 6% APR, €190 minimum

With €200 extra per month, avalanche directs it to Card A first, then Card B, then the auto loan. You’ll save the most interest with this sequence.

Debt Snowball (Psych-First)

With the snowball, you pay minimums on everything and throw all extra cash at the smallest balance. When it disappears, you roll its entire payment into the next-smallest balance. The quick win releases motivation and confidence especially useful if you’ve felt stuck or overwhelmed.

Same example, snowball order: Card B (€1,400) → Card A (€2,200) → Auto (€6,800). You may pay a bit more interest but gain momentum sooner.

Which Method Should You Pick?

- Choose avalanche if you’re numbers-driven and motivated by minimizing interest.

- Choose snowball if motivation is your bottleneck and you crave early victories.

Pro tip: If you start with snowball for momentum, you can later switch to avalanche once you feel confident. It’s not either/or forever. You’re allowed to adapt.

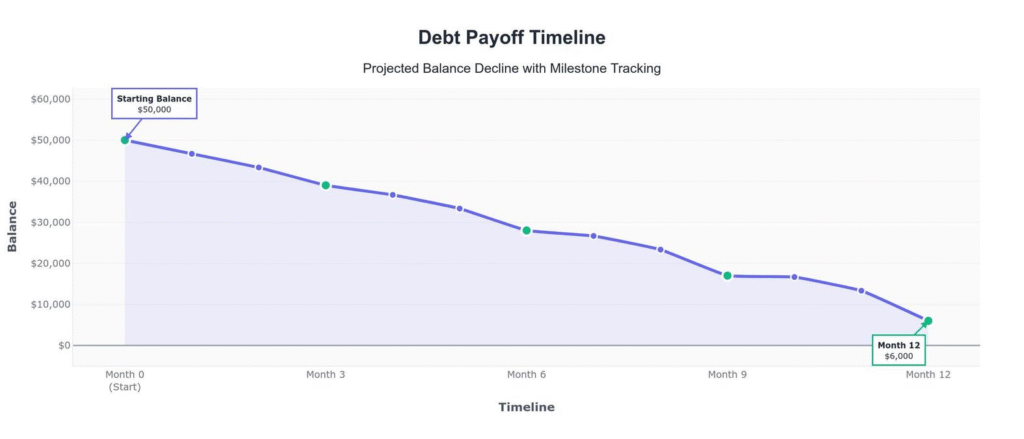

Turn Your Goals into a Payoff Timeline You Can Live With

Once you’ve chosen your method, translate it into a month-by-month schedule. A plan transforms hope into execution. It also protects your energy: when the path is visible, you’re less likely to panic during setbacks or spend impulsively.

Step-by-Step Timeline Builder

- Set a target debt-free date: Ambitious but realistic (e.g., 18–36 months).

- Calculate your baseline surplus: Income minus essential expenses and modest sinking funds (car maintenance, annual fees, etc.).

- Assign your surplus: Minimums on all loans + all extra to your current target debt (avalanche/snowball).

- Plot milestone balances: Predict where each debt will stand in 3, 6, 9, and 12 months.

- Add seasonal boosts: Tax refund, bonus, or a one-time sell-off to “jump” a milestone.

Tip: Use conservative assumptions. If your plan works under cautious estimates, real life pleasantly surprises you.

Beginner note: perfection isn’t required. If an unexpected expense slows you down, you didn’t fail you just update the plan and keep moving. Progress > perfection.

Free Up Cash with Budget Tweaks That Don’t Feel Like Punishment

Paying extra is easier when you find extra. You don’t need to overhaul your life. Small, painless savings stack quickly and can knock months off your payoff date. The trick is to reduce friction, not joy.

High-Yield Quick Wins

- Subscriptions audit: Cancel just one underused subscription (€10–€20 monthly) and auto-redirect it to your target loan.

- Insurance re-shop: Compare policies annually; modest savings (€15–€40/month) add up.

- Meal planning lite: Plan three dinners a week; reduce delivery by one order/week.

- Utility hygiene: Thermostat tweaks, LED bulbs, and unplugging vampire devices.

- “No-spend” weekdays: Choose Mon–Thu for coffee at home; indulge on weekends guilt-free.

Micro-Income Boosters

- Sell forgotten items: Old tech, furniture, designer clothing. Send 100% of proceeds to debt.

- One small side hustle: Deliveries, tutoring, design gigs. Dedicate a set percentage to loans.

- Employer perks: Expense reimbursements and stipends free up personal cash for payoff.

Behavioral trick: create a dedicated “Debt Accelerator” account. Any savings or side income lands there automatically, then sweeps to your target loan monthly. Keeping it separate prevents accidental spending.

Slash Interest Legally with Refinancing, Consolidation and Balance Transfers

Interest is the price of time. Lower it, and your payoff speeds up even if your payment stays the same. Use refinancing and consolidation to reduce APRs, simplify payments, or both, while watching for traps that make debts last longer than necessary.

Refinancing vs. Consolidation

- Refinancing: Replace one loan with a new loan at a lower APR (or shorter term). Ideal for auto or personal loans.

- Consolidation: Roll multiple debts into one loan. Helpful for simplicity and possibly lower blended interest.

Balance Transfers (for Credit Cards)

Many cards offer 0% intro APR on transfers for 6–21 months. This can be a powerful bridge—if you pay down aggressively before the promo ends. Watch for 3–5% transfer fees and the revert APR once the period ends.

Smart Rules of Thumb

- Seek a lower APR without adding excessive fees.

- Prefer shorter or equal terms. Avoid stretching debt so long that total interest increases.

- Do not use newly freed credit lines for new spending.

Mini-case study: Ben has €7,500 on a card at 24% APR. He transfers to a 0% card for 15 months with a 3% fee (€225). He automates €500/month. In 15 months he pays €7,500 + €225 fee, saving over €1,000 in interest versus keeping the balance at 24%.

[EXTERNAL LINK: source-name] “Comparing APRs and total cost of credit”

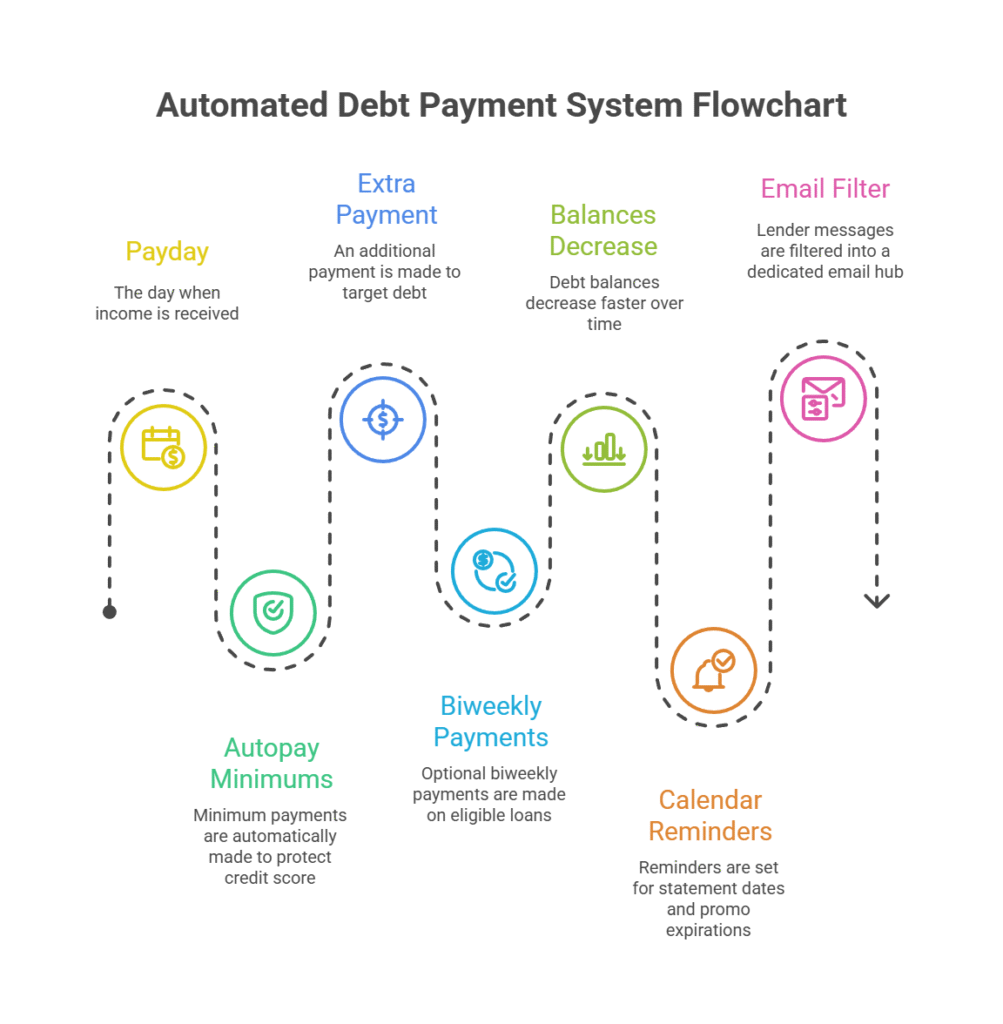

Automate Everything You Can to Remove Willpower from the Equation

Consistency beats intensity. Automation turns your plan into a set of defaults. Payments happen even on busy weeks, and you avoid late fees or missed due dates. Done right, automation also smooths your cash flow and reduces money anxiety.

Automation Checklist

- Autopay minimums on every loan to protect your credit score.

- Schedule an automatic extra payment to the current target debt the day after payday.

- Set calendar reminders for statement dates, promo expirations, and APR changes.

- Create a “bill hub” email filter so lender messages never get buried.

Biweekly Payments (When Allowed)

For some installment loans (mortgage, auto), switching to biweekly payments subtly accelerates payoff: 26 half-payments = 13 full payments per year. Always confirm with your lender to ensure extra payments hit principal, not future interest.

Negotiate with Lenders Because It Works More Often Than You Think

Lenders prefer on-time payments to collections. If you’re proactive and polite, many will cooperate by reducing APRs, waiving fees, or offering hardship programs. The earlier you communicate, the better your options.

What to Ask For

- Rate reduction: “I’m a long-time customer. Can you review my account for a lower APR?”

- Fee waiver: One-off late fee forgiveness if you’re usually on time.

- Hardship plan: Temporary lower payments or interest while you stabilize.

- Re-age the account: For certain loans, bringing delinquent accounts current after consecutive on-time payments.

Negotiation Script (Template)

“Hi, I’m calling about my account ending in 1234. I want to stay in good standing and pay this off quickly. Given my on-time history and current budget, can you help me lower my APR or waive last month’s fee? I’m committed to consistent payments and would appreciate any flexibility you can offer.”

Track outcomes in your debt inventory. Even a 2–4% APR drop can shave months off your timeline.

Pay Faster Without Burning Out by Building a Two-Tier Plan

Debt fatigue is real. A plan that ignores joy or margin is a plan that dies in month three. Avoid the boom-and-bust cycle by designing two speeds: Baseline and Accelerated.

Baseline Plan (Always Achievable)

- Minimums on all loans + a fixed, manageable extra (e.g., €75/month).

- Budget still funds modest fun, savings buffers, and essentials.

- Confidence stays high because you consistently hit the target.

Accelerated Plan (Opportunity Mode)

- Any surplus from overtime, side gigs, tax refunds, or selling items.

- Seasonal lump sums mapped in advance.

- Temporary “sprint months” followed by “maintenance months.”

This flexible structure prevents guilt and burnout. You’re not failing if you only hit the baseline. You’re succeeding. Acceleration is a bonus that compounds your progress.

Stay Motivated by Building Systems, Rituals and Quick Wins

Debt repayment is a long game. Motivation spikes at the start and dips in the middle. Use psychology to keep momentum steady.

Build a Motivation Engine

- Visual tracker: A thermometer chart or debt-free countdown on your fridge or desktop.

- Milestone rewards: After every €1,000 paid, treat yourself (budgeted, small).

- Identity shift: “I’m the kind of person who pays off debt quickly and calmly.”

- Community: Share wins with a friend or accountability group.

Mini-case study:

Priya set a 24-month plan with a colored bar chart on her wall. Each €500 chunk turned a new segment green. The visual satisfaction made the process feel like a game. She finished in 20 months.

Protect Your Progress with Emergency Funds, Sinking Funds and Risk Management

Speed matters, but stability matters more. Aggressive payoff without a buffer can backfire. One unexpected expense and you’re back on high-interest credit. Build small safety nets to defend your progress.

Emergency Fund (Starter)

- Goal: €500–€1,500 while paying off high-interest debt; grow later.

- Use only for: Medical, car repairs, essential bills—not vacations or gadgets.

Sinking Funds

Save small amounts monthly for predictable but non-monthly expenses: car maintenance, holidays, annual subscriptions, gifts. This stops these costs from derailing your payoff plan.

Think of these funds as shock absorbers; they let you accelerate without wrecking your timeline on the first bump.

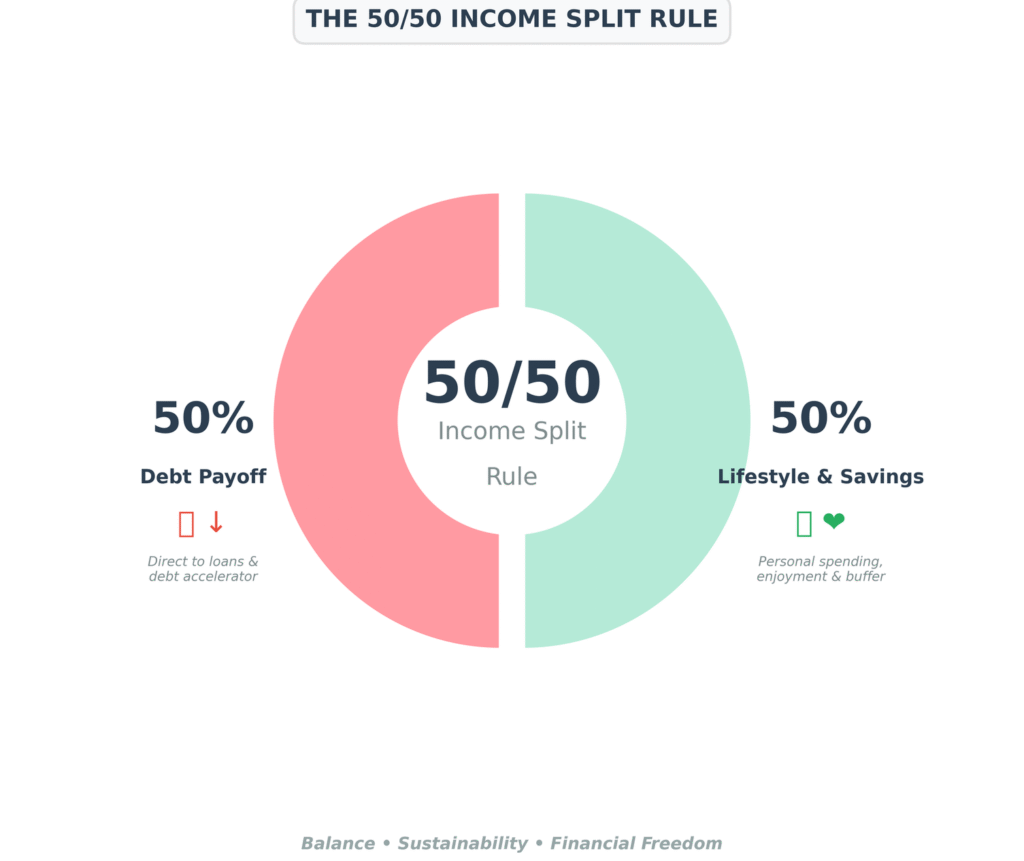

Use Side Income Ethically with the 50/50 Split

Side income can slash months off your payoff date. The catch: many people earn more and then spend more. A practical rule is the 50/50 split: send 50% of any new income straight to your target loan and keep 50% for lifestyle or savings. That way, you feel rewarded and you accelerate debt. Sustainable beats extreme.

Beginner-Friendly Side Gigs

- Freelance skills: writing, design, editing, coding.

- Local services: tutoring, pet sitting, yard work.

- Micro-jobs: deliveries, user testing, short surveys.

Automate the 50% transfer from your side-gig account to your “Debt Accelerator” account every payday. Less willpower, more progress.

Handle Variable or Irregular Income with Tiered Minimums

If your income fluctuates, use “tiered minimums.” Define three monthly budgets: Lean, Normal, and High. Each tier has a pre-decided extra payment so you never have to decide under pressure.

Example Tiers

- Lean month: Minimums + €25 extra

- Normal month: Minimums + €125 extra

- High month: Minimums + €300 extra

This system protects your plan during slow months and capitalizes on strong months without guilt or decision fatigue.

Avoid Common Mistakes and Protect Your Progress

Learning from others’ mistakes is the fastest way to stay out of trouble. Here are the big ones plus the fix.

- Only paying minimums forever: Fix by auto-scheduling a small extra payment (even €20 helps).

- Ignoring APRs: Fix by listing rates and using avalanche on the costliest debt.

- Stretching consolidation too long: Fix by choosing equal/shorter term to reduce total interest.

- New spending after a balance transfer: Fix by freezing old cards or using them strictly for a small monthly bill you pay in full.

- No buffer: Fix by keeping a starter emergency fund so surprises don’t go on credit.

- All-or-nothing mentality: Fix by adopting baseline + accelerated tiers to prevent burnout.

Use Tools and Trackers to Make Progress Visible

What gets measured gets managed. Use simple tools to keep your plan on track.

Essentials

- Debt payoff spreadsheet: Tracks balances, APRs, targeted extra payments.

- Calendar reminders: Statement dates, promo expirations, milestones.

- Note-taking app: Negotiation logs, lender call outcomes, reference numbers.

Nice-to-Have

- Progress visualizer: Bar or thermometer chart.

- Automation rules: Bank rules that sweep funds to loans after payday.

- Habit tracker: “No-spend weekdays,” “weekly statement check,” “side-gig hours.”

Mini Case Studies that Show Realistic Paths to Faster Payoff

Case Study 1: The One-Card Avalanche

Profile: Alex has a single credit card (€3,400 @ 23% APR). He can spare €175 extra/month.

Plan: Avalanche (only one debt). Autopay minimum + €175 scheduled the day after payday.

Result: Pays off in ~17 months, saving hundreds in interest versus minimums alone. Motivation stays high because progress is visible monthly.

Case Study 2: The Snowball Starter

Profile: Sam has three debts: €900, €1,800, and €6,200 (APRs 19%, 14%, 7%).

Plan: Snowball for psychology, kill €900 first within three months, then roll the freed payment into €1,800.

Result: The early win flips Sam from avoidance to action. After the first two debts fall, Sam switches to avalanche for the final loan.

Case Study 3: The Refinancer

Profile: Lina’s car loan is €11,500 @ 10.5%.

Plan: Refinance to 6.2% with equal term; keep payment the same.

Result: Interest drops sharply, the payoff date moves closer, and Lina redirects the savings to a high-APR card.

These stories highlight a theme: there isn’t a single “right” path—there’s the path you’ll follow consistently.

Consider Your Credit Score While You Pay Down Debt

As balances fall and on-time payments stack up, your credit profile usually improves. A stronger score can yield lower insurance premiums, cheaper loans, and higher approval odds. Handle the journey thoughtfully to keep the score trending up.

Levers That Matter

- Payment history: Never miss a due date—autopay minimums as insurance.

- Utilization: Keep revolving balances low; pay before the statement date for best effect.

- Length of history: Avoid closing your oldest no-fee accounts.

- New credit: Batch applications sparingly; too many inquiries can ding scores short term.

As your score rises, you may qualify for better refinance terms—another compounding win for your payoff timeline.

Stay Debt-Free After the Last Payment Clears

Reaching zero is thrilling and a pivotal moment to lock in your progress. Before lifestyle creep returns, redirect your former debt payments to long-term goals.

The Post-Debt Playbook

- Finish your full emergency fund: 3–6 months of essential expenses.

- Attack a single savings goal: Car replacement fund, home down payment, or education fund.

- Invest consistently: Automate contributions to retirement and index funds. https://investwisetoday.com/cryptocurrency-investing-for-beginners-2025/

- Use credit cards strategically: Pay in full, keep utilization low, redeem rewards smartly.

Debt freedom isn’t just about what disappears, it’s about the options that appear.

Frequently Asked Questions

1) Should I pay off loans or build savings first?

Keep a small emergency buffer (often €500–€1,500) while attacking high-interest debt. That cushion prevents you from putting surprise expenses back on a card. After high-APR debt is gone, build a full 3–6 month emergency fund before ramping up investing. Your risk tolerance and job stability may shift these ranges slightly.

2) What if I can only make minimum payments?

Start with the smallest possible extra—€10–€25—to build momentum, then hunt for one painless budget cut or one micro-gig. Small extras make a big difference over time, especially on high APRs. Automate the extra the day after payday so it doesn’t get spent.

3) Are debt consolidation loans a good idea?

They can be if the new APR is lower, fees are reasonable, and the term isn’t stretched so long you pay more total interest. The goal is lower cost and similar/shorter timeline, not just a lower monthly payment. Run the numbers first.

4) Does refinancing hurt my credit?

There’s usually a small, temporary dip from a hard inquiry and a new account, but on-time payments and lower utilization often outweigh it. If refinancing cuts interest and accelerates payoff, the long-term benefit is typically worth the brief score impact.

5) How many balance transfers are too many?

Use them sparingly and strategically. Each new card can add inquiries and tempt new spending. If you do a transfer, freeze or strictly limit use of the transferred-from card, and set a schedule to clear the balance before the promo ends.

Conclusion, Consistency Wins the Debt Game

Paying off loans faster doesn’t require perfection, extreme deprivation, or a sudden windfall. It requires clarity (know exactly what you owe), a method (avalanche or snowball), and consistency (automate the next right payment). Add selective interest reduction (refinance or transfer when it truly helps), a two-tier plan to avoid burnout, and simple trackers that make progress visible and you have a system that works in the real world.

The moment you commit to the plan, your debt stops being a vague stressor and becomes a project with a finish line. Every month you pay, the finish line moves closer. Celebrate small wins, protect your energy, and keep going.

Call to Action. Take Three Actions Right Now

1) Build your one-page debt inventory.

2) Choose avalanche or snowball and schedule your extra payment for the day after payday.

3) Cancel or reshop one monthly expense and auto-redirect the savings to your target loan.

Start small today. In a few months, you’ll feel the momentum. In a year, you’ll see the transformation. And when the last payment clears, you’ll own your paycheck again.