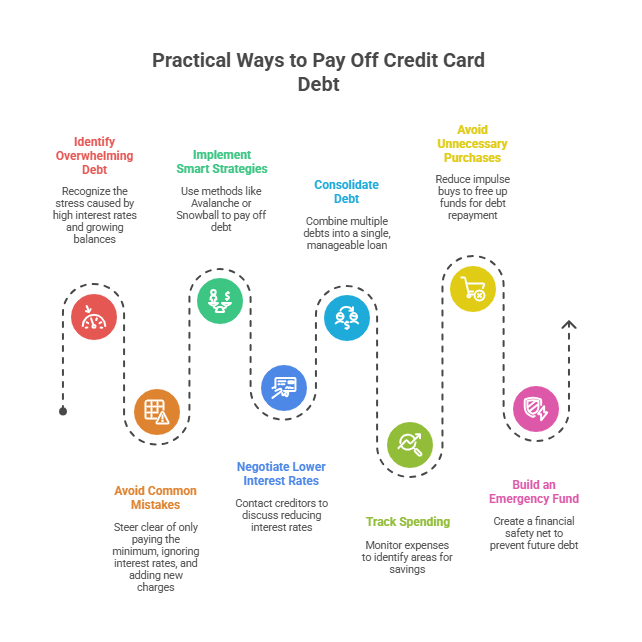

Credit card debt can feel overwhelming, but with the right strategies, you can take control and start paying it off faster. Many beginners make common mistakes like only paying the minimum or ignoring interest rates. This comprehensive guide provides step-by-step strategies to manage and eliminate your debt while keeping your finances healthy and building long-term financial habits.

Why Paying Off Credit Card Debt Matters

Why Paying Off Credit Card Debt Matters

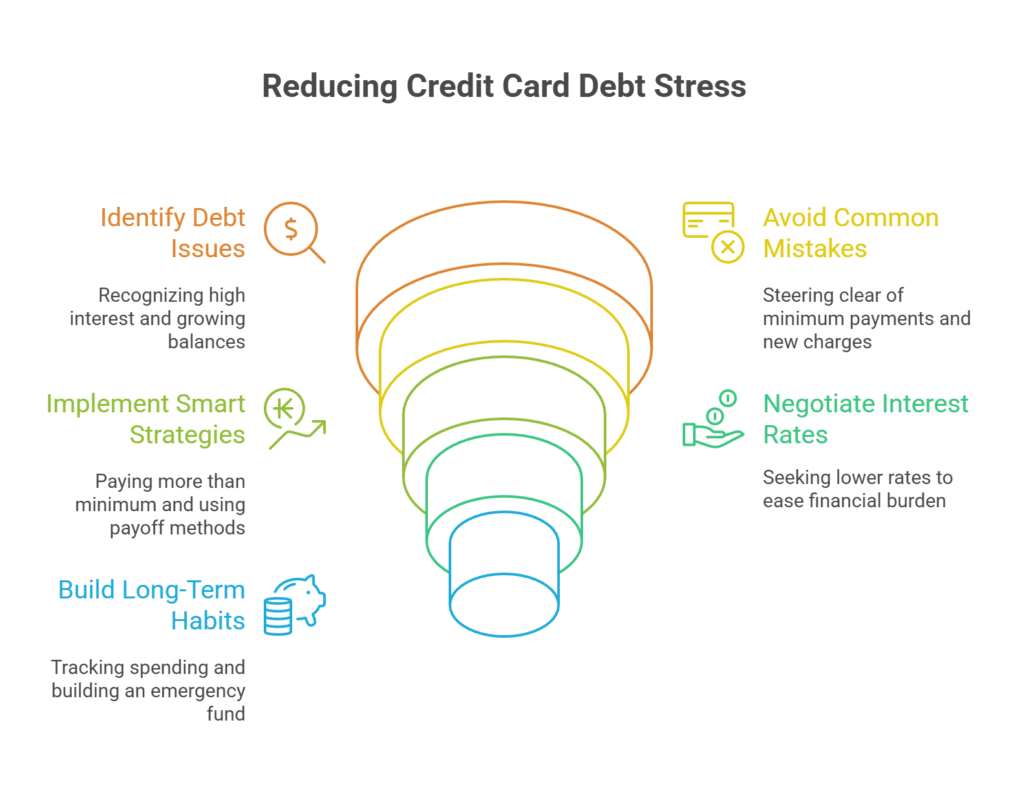

Carrying high-interest credit card debt can become a significant financial burden if ignored. Paying off debt quickly not only saves money on interest but also improves your credit score, reduces stress, and allows you to regain control of your finances. The sooner you start, the more you can benefit from strategic debt management.

Interest Rates Are Expensive

Most credit cards charge an Annual Percentage Rate (APR) between 15% and 25%. Paying only the minimum each month dramatically extends the repayment period and can cost thousands in additional interest over time. For instance, a $2,000 balance at 20% APR could take years to pay off if only minimum payments are made. Tools can help you visualize repayment timelines and interest accumulation.

Impact on Credit Score

Credit utilization is the ratio of your balances to credit limits directly affects your credit score. High utilization lowers your score, making it harder to qualify for loans or favorable credit terms. Financial experts recommend keeping credit utilization below 30% on all cards. Paying down balances consistently is one of the fastest ways to improve your score and strengthen your overall financial profile.

Step-by-Step Strategies to Eliminate Debt

Paying off credit card debt requires planning, discipline, and actionable strategies. The following steps are designed for beginners but are effective for anyone looking to regain control of their finances.

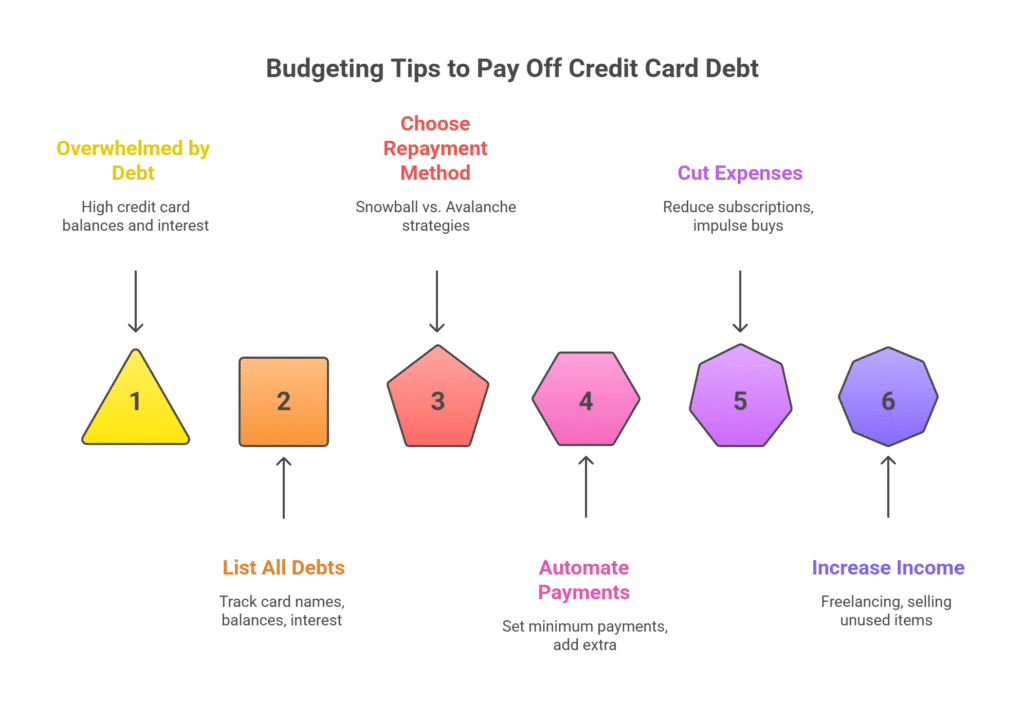

1. List All Debts

Begin by creating a comprehensive list of all your credit cards, balances, interest rates, and minimum payments. This step provides clarity on the scope of your debt and helps identify which balances need urgent attention. You can use budgeting apps or spreadsheets to track this information efficiently. Include the following details for each card:

- Card name and issuer

- Current balance

- Minimum monthly payment

- Interest rate (APR)

- Due dates

Having a clear overview helps you prioritize payments, track progress, and prevent any balances from falling through the cracks.

2. Choose a Repayment Method

Two popular debt repayment strategies are widely used:

- Debt Snowball: Focus on paying off the smallest balance first while making minimum payments on other cards. This method builds momentum and motivation as each balance is eliminated.

- Debt Avalanche: Focus on paying off the highest-interest debt first to save the most money on interest over time. Minimum payments are made on other cards.

For beginners, the debt snowball approach is psychologically rewarding and helps maintain motivation. The debt avalanche method is mathematically optimal for minimizing total interest paid. Choose the method that best suits your financial personality and goals.

3. Automate Payments

Setting up automatic payments ensures you never miss a due date, avoiding late fees and credit score damage. Automation is particularly effective for minimum payments, while additional manual payments can be added when extra cash is available. Here’s how to implement automated repayment:

- Link your bank account to each credit card.

- Schedule automatic minimum payments each month.

- Allocate additional funds toward your target debt card.

- Track all payments monthly to ensure accuracy and adjust as needed.

Consistency is crucial. Even small extra payments accelerate debt payoff and reduce total interest substantially.

4. Cut Expenses to Free Up Cash

Review your monthly budget and identify areas to reduce spending. Freeing up cash allows more money to go directly toward debt repayment. Practical strategies include:

- Reducing dining out and takeout expenses

- Canceling unnecessary subscriptions

- Limiting impulse purchases or luxury items

- Using cashback or rewards programs strategically

- Shopping smarter with lists and budgeting tools

Even modest savings of $50–$100 per month can dramatically shorten the time it takes to pay off a balance when consistently applied. Small lifestyle adjustments have a big impact over time.

5. Increase Your Income

Boosting your income accelerates debt repayment. Consider options such as:

- Freelance work in your skill area https://www.upwork.com/

- Part-time or gig economy jobs

- Selling unused items online

- Monetizing hobbies or crafts

- Participating in referral programs

Direct any extra earnings straight to your debt. While this requires discipline, the payoff is significant, reducing both time and interest costs.

Advanced Tips for Faster Progress

Once the basics are in place, these advanced strategies can further accelerate repayment and improve your financial habits.

Balance Transfers

Some credit cards offer 0% introductory APR on balance transfers for a limited period. Transferring high-interest debt to such cards allows you to pay off the principal faster without accruing additional interest. Key considerations:

- Check transfer fees (typically 3–5% of the balance)

- Note the length of the promotional period

- Ensure you can pay off the balance before the rate increases

- Use tools to calculate potential savings

Negotiate Interest Rates

Contact your credit card issuer to request a lower APR. Many companies are willing to reduce rates for customers with good payment histories. A small reduction in APR can save hundreds of dollars over the course of repayment.

Track Progress and Celebrate Milestones

Monitor your debt reduction regularly. Celebrate achievements such as:

- Paying off a credit card completely

- Reducing total debt by 25% or 50%

- Lowering overall interest payments

Tracking progress visually through charts or apps keeps motivation high and encourages continued diligence.

Common Mistakes to Avoid

Using New Credit Cards

Avoid opening or using new credit cards while paying off existing balances. Accumulating new debt undermines your repayment plan and extends the timeline to financial freedom.

Ignoring Minimum Payments

Missing minimum payments leads to late fees, higher interest rates, and credit score damage. Set up automation to ensure at least minimum payments are made each month.

Overcomplicating the Plan

Keep your repayment strategy simple. Pick a method (snowball or avalanche) and stick to it. Consistency, rather than complexity, is what drives results.

Frequently Asked Questions

1) Can I pay off debt with just extra savings?

Yes, but maintain a small emergency fund to cover unexpected expenses. This prevents reliance on credit cards and avoids increasing your debt while paying it down.

2) Should I close paid-off cards?

Not immediately. Keeping accounts open helps maintain a long credit history and favorable credit utilization. Closing accounts too early can inadvertently lower your credit score.

3) How long will it take to be debt-free?

The timeline depends on your total balances, interest rates, and extra payments. Many beginners pay off moderate debt within 12–24 months with consistent effort.

4) Are balance transfer cards safe?

Yes, if you understand the terms. Ensure you can pay off the balance before the promotional period ends and avoid accumulating new debt on other cards.

5) Can I combine strategies?

Absolutely. Using a combination of expense reduction, automation, and extra income strategies accelerates debt payoff and builds good financial habits.

Takeaways

Paying off credit card debt quickly is achievable with a structured approach. By listing debts, choosing a repayment method, automating payments, cutting expenses, and increasing income, you can regain control of your finances. Advanced tactics like balance transfers, negotiating interest rates, and tracking milestones can further accelerate progress. Avoid common pitfalls such as accumulating new debt or ignoring minimum payments. With discipline, patience, and strategic action, you can eliminate debt and build a strong foundation for long-term financial health.

Start today by creating your debt list, automating payments, and identifying areas to free up cash. Your future self will thank you.