In 2025, financial literacy is more crucial than ever. Whether you’re building a foundation for financial stability, paying off debt, or simply trying to manage your day-to-day spending, mastering your monthly budget is the key to long-term financial success. Budgeting doesn’t have to feel restrictive or complicated when done right, it’s empowering. This comprehensive guide will walk you through every step of creating, managing, and maintaining a realistic budget that works for your life.

By the end of this guide, you’ll have the tools and knowledge to take full control of your finances, set clear goals, and start making confident financial decisions without feeling overwhelmed.

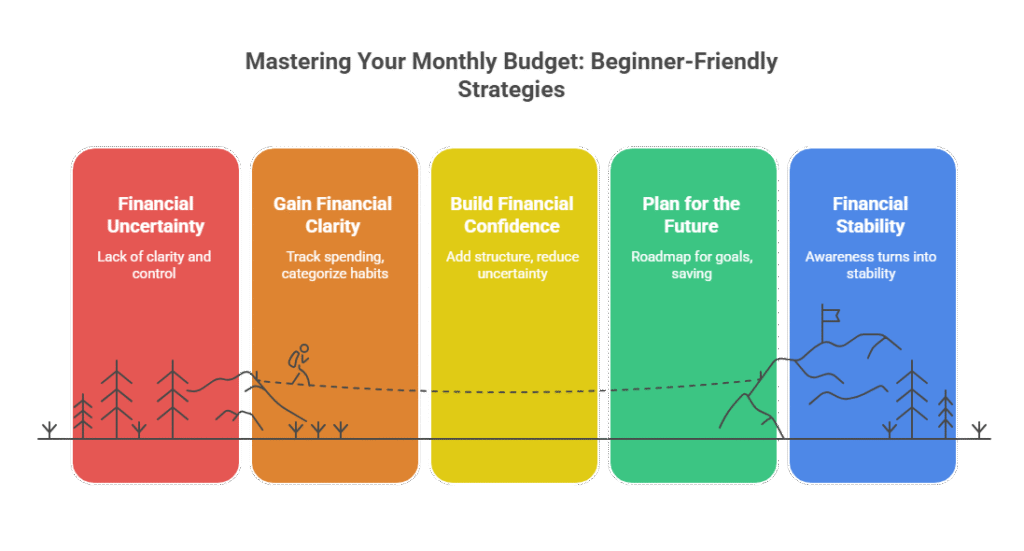

Why Budgeting Matters

At its core, budgeting is about control and clarity. It’s not about limiting yourself, it’s about making sure every dollar you earn has a purpose. Whether your goal is to build savings, pay off debt, or simply feel more confident with money, budgeting gives you the structure and insight to make it happen.

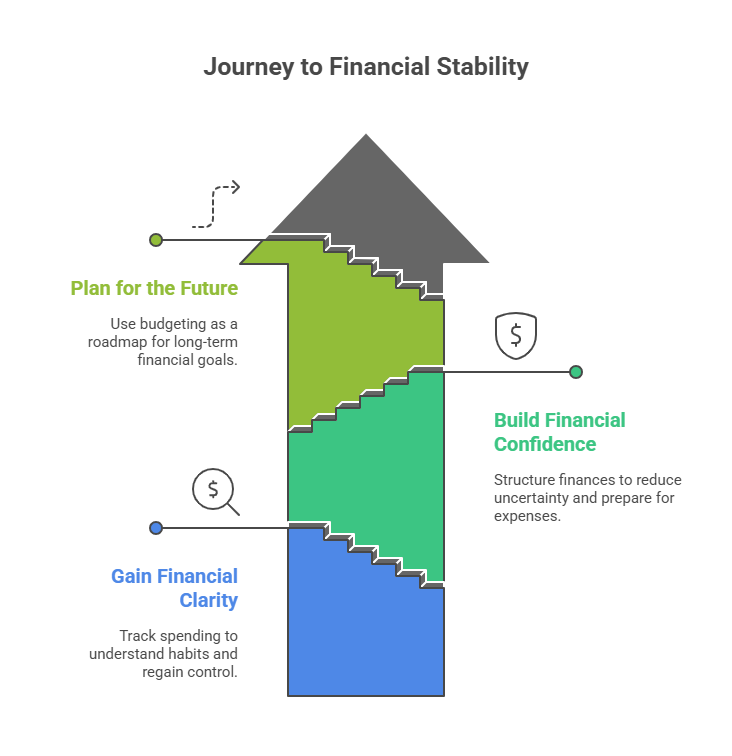

1. Gain Financial Clarity

Most people underestimate how much they spend each month. A budget gives you a clear view of where your money is going. When you categorize expenses; such as housing, groceries, transportation, entertainment, and savings. You gain awareness of spending habits that may otherwise go unnoticed.

With clarity comes control. Once you understand your spending patterns, you can identify unnecessary costs and redirect funds toward your priorities, such as building an emergency fund or investing for the future.

2. Build Financial Confidence

Creating a budget is a confidence booster. It replaces uncertainty with structure and helps you make informed decisions. You’ll feel more secure knowing you’re prepared for bills, savings goals, and unexpected expenses. Over time, this confidence builds discipline. A key ingredient for long-term financial success.

3. Plan for the Future

Budgeting isn’t just about surviving month to month. It’s about creating a financial roadmap. Whether your goal is to save for a home, plan for retirement, or fund travel experiences, a budget helps you allocate resources strategically and track progress toward those milestones.

Step-by-Step Guide to Building a Monthly Budget

Creating a monthly budget doesn’t require advanced math or complex tools. All it takes is consistency, awareness, and a willingness to adjust as you go. Follow these five practical steps to get started:

Step 1: Calculate Your Income

Your income is the foundation of your budget. List every reliable source of income you receive each month. This includes your salary, freelance earnings, side hustles, and passive income. Be sure to focus on your net income (after taxes), not your gross pay, to avoid budgeting with unrealistic numbers.

Tip for freelancers or gig workers: If your income fluctuates, calculate your average monthly income over the last 6–12 months. Then, plan your budget based on that conservative estimate.

Step 2: Track Your Expenses

Tracking your expenses helps you see how your spending aligns with your priorities. Start by categorizing your expenses into three groups:

- Fixed expenses: Rent or mortgage, insurance, utilities, and loan payments.

- Variable expenses: Groceries, transportation, entertainment, and personal spending.

- Discretionary expenses: Non-essentials such as dining out, subscriptions, or hobbies.

You can track expenses manually using a spreadsheet, or use a free budgeting app like [affiliate:BudgetApp] to automate tracking and generate reports that visualize your cash flow.

Step 3: Set Clear Financial Goals

Budgets are more meaningful when connected to specific goals. Define short-term and long-term objectives, like saving $1,000 for an emergency fund, paying off a credit card, or setting aside money for a vacation.

Example: If your goal is to save $3,000 in a year, divide it by 12 months. You’ll need to save $250 per month. Visualizing your goals this way makes them feel achievable.

Consider setting SMART goals; Specific, Measurable, Achievable, Relevant, and Time-bound. For instance, instead of saying “I want to save more money,” say “I will save $250 monthly for 12 months to build an emergency fund.”

Step 4: Create Your Spending Plan

Once you know your income and expenses, it’s time to allocate funds to each category. Start with essentials like rent, food, and utilities. Then allocate to savings and debt repayment before adding discretionary spending.

A popular method is the 50/30/20 rule:

- 50% of income → needs (housing, food, bills)

- 30% → wants (dining out, hobbies, entertainment)

- 20% → savings and debt repayment

This flexible framework helps maintain balance while still allowing room for enjoyment.

Step 5: Review and Adjust Regularly

Budgets are not static, they evolve as your financial situation changes. Review your budget weekly or monthly to ensure it still reflects your current income, goals, and lifestyle. Adjust when necessary like after a salary change or unexpected expense—to stay on track.

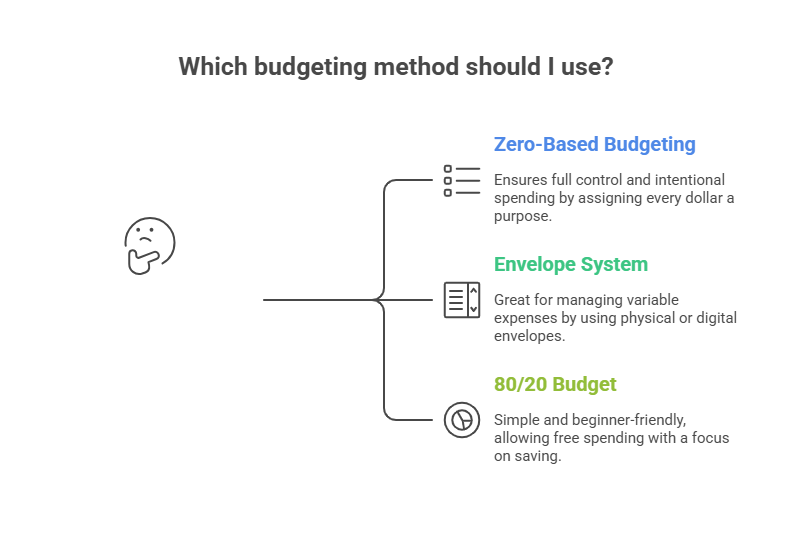

Essential Budgeting Techniques for Beginners

1. Zero-Based Budgeting

With zero-based budgeting, every dollar you earn is assigned a purpose. At the end of each month, your income minus your expenses equals zero. This doesn’t mean you have no money left, it means every dollar is allocated intentionally, whether it’s for bills, savings, or investments.

For example, if you earn $3,000 monthly, your goal is to distribute that amount across all categories until nothing remains unassigned.

2. Envelope System

This classic budgeting technique uses physical envelopes (or digital equivalents) for each spending category. Once an envelope’s money is gone, you stop spending in that category for the month. It’s an effective way to manage variable expenses like groceries or entertainment.

3. The 80/20 Budget

If you prefer simplicity, try the 80/20 method; save or invest 20% of your income and freely spend the remaining 80% as needed. It’s ideal for beginners who want a low-maintenance budget that still encourages savings.

Practical Tips for Sticking to Your Budget

Even the best budget is useless if you don’t stick to it. Here are some proven strategies to stay consistent:

Automate Savings

Set up automatic transfers to your savings account right after payday. This “pay yourself first” strategy removes temptation and ensures you build savings effortlessly.

Use Budgeting Tools and Apps

Technology can simplify your budgeting journey. Free tools like [affiliate:BudgetApp] or Google Sheets make it easy to monitor spending patterns, set reminders, and visualize progress. These apps also sync with your bank accounts, making tracking seamless and accurate.

Review Subscriptions and Recurring Charges

One of the easiest ways to save money is by canceling unused subscriptions. Audit your recurring charges every few months to identify services you no longer use.

Practice Mindful Spending

Before making a purchase, ask yourself: “Do I need this, or do I just want it?” A moment of reflection can help prevent impulse buys and strengthen financial discipline over time.

Common Beginner Mistakes (and How to Avoid Them)

1. Ignoring Small Expenses

Many people underestimate the impact of minor purchases. Daily coffees, snacks, or subscriptions can quietly drain your budget. Track every expense, no matter how small it’s often the small leaks that sink the ship.

2. Being Too Restrictive

Budgets should be realistic, not punishing. Allow some flexibility for fun and relaxation. Overly strict budgets often lead to burnout and overspending later.

3. Forgetting Irregular Expenses

Plan for non-monthly expenses like insurance renewals, gifts, or annual memberships. Setting aside a small amount each month prevents surprises when those bills arrive.

4. Not Reviewing Your Budget

Your financial situation will change. Failing to review your budget means missing opportunities to optimize. Regularly updating it ensures it continues serving your needs.

Advanced Budgeting Tips for 2025

Once you’ve mastered the basics, you can take your budgeting strategy to the next level by incorporating long-term planning and wealth-building techniques.

1. Track Net Worth

Beyond monthly cash flow, start tracking your overall net worth assets minus liabilities. This gives a more complete view of your financial health and progress over time.

2. Build an Emergency Fund

Set aside at least 3–6 months’ worth of essential expenses in an accessible account. This safety net prevents you from relying on credit cards during emergencies.

3. Automate Investments

Once you’ve established savings habits, consider automating investments in low-cost index funds or retirement accounts. Start small, but stay consistent. Automation helps you build wealth passively.

4. Review Financial Goals Quarterly

Revisit your goals every few months to ensure they align with your current priorities. Adjust savings targets or spending categories as your life evolves.

[LINK: related-post] [EXTERNAL LINK: Investopedia Budgeting Basics]

Budgeting for Irregular Income

If you’re a freelancer, contractor, or gig worker, budgeting can feel unpredictable. The key is consistency and cautious planning. Here’s how to handle irregular income effectively:

- Average your income: Calculate your earnings from the past 6–12 months and use that as your baseline.

- Prioritize essentials: Pay rent, food, and utilities first, then allocate toward savings and discretionary spending.

- Build a buffer: During high-income months, save extra to cover slower periods.

Tools make it easy to monitor variable income and adapt your spending accordingly.

Frequently Asked Questions

1. How much should I save each month?

Aim to save at least 20% of your net income if possible. However, if that feels too high, start smaller, what matters is building the habit. Gradually increase your savings rate over time.

2. Can I budget if I’m living paycheck to paycheck?

Yes. Start by tracking your expenses for a month to identify where small cuts can be made. Even saving $20–$50 per paycheck can help you build momentum.

3. Should I use cash or cards for budgeting?

Both can work. Cash-based systems like the envelope method help control spending, while digital tools provide convenience and analytics. Choose what fits your lifestyle best.

4. How often should I review my budget?

At least once a month. Regular reviews help you adjust to changes, catch overspending early, and celebrate small wins along the way.

5. What’s the best budgeting app for beginners?

Apps like https://www.everydollar.com/ are great for beginners, they automate tracking, categorize expenses, and help visualize spending patterns with minimal effort.

Takeaways

Mastering your monthly budget isn’t about restriction it’s about empowerment. A well-structured budget helps you take control of your finances, reduce stress, and plan confidently for the future. Whether you’re saving for a goal, paying off debt, or simply trying to spend more mindfully, the journey begins with awareness and consistency.

Start small, use free tools to track your progress, and adjust as you learn. Over time, you’ll not only manage your money better you’ll feel more secure, independent, and ready for whatever financial challenges come your way.

Take the first step today. Create your budget, commit to it, and watch how small, consistent actions transform your financial future.