When it comes to building long-term wealth, two of the most popular and effective investment vehicles are index funds and exchange-traded funds (ETFs). Both provide investors with broad market exposure, diversification, and low fees, all essential ingredients for growing wealth steadily over time. But despite their similarities, there are key differences that can significantly impact your investment strategy, taxes, and overall returns.

This comprehensive guide will help you understand exactly how index funds and ETFs work, their pros and cons, and which one may be a better fit for your long-term investing goals. Whether you’re just getting started or refining an existing portfolio, this deep dive will help you make confident, informed choices.

Understanding the Basics

What Is an Index Fund?

An index fund is a type of mutual fund designed to replicate the performance of a specific market index, such as the S&P 500, NASDAQ 100, or Dow Jones Industrial Average. Instead of hiring fund managers to pick individual stocks, the fund simply buys shares of all (or most) of the companies in the chosen index, automatically matching its performance. This passive investing approach eliminates the need for constant management, and that translates into lower fees for investors.

For example, if you invest in an S&P 500 index fund, your money is spread across 500 of the largest U.S. companies. When Apple, Microsoft, or Amazon perform well, your fund’s value rises. When they fall, your value drops. But because you own a tiny piece of hundreds of companies, no single stock can devastate your entire portfolio.

What Is an ETF?

An exchange-traded fund (ETF) is also designed to track a market index, sector, or asset class, but unlike index funds, ETFs trade on stock exchanges throughout the day, just like individual stocks. This means you can buy and sell shares of an ETF whenever the market is open, with prices that fluctuate in real time.

ETFs were first introduced in the 1990s and have exploded in popularity due to their flexibility, transparency, and low costs. Some of the most popular ETFs include the SPDR S&P 500 ETF (SPY), Vanguard Total Stock Market ETF (VTI), and iShares MSCI Emerging Markets ETF (EEM).

Essentially, ETFs are like index funds with extra flexibility. They offer the same broad diversification but are easier to trade and often come with slightly lower expenses.

Key Differences Between Index Funds and ETFs

Although both aim to track market indexes and offer low-cost diversification, there are several important differences in how they operate. Understanding these distinctions will help you choose the right investment vehicle for your strategy.

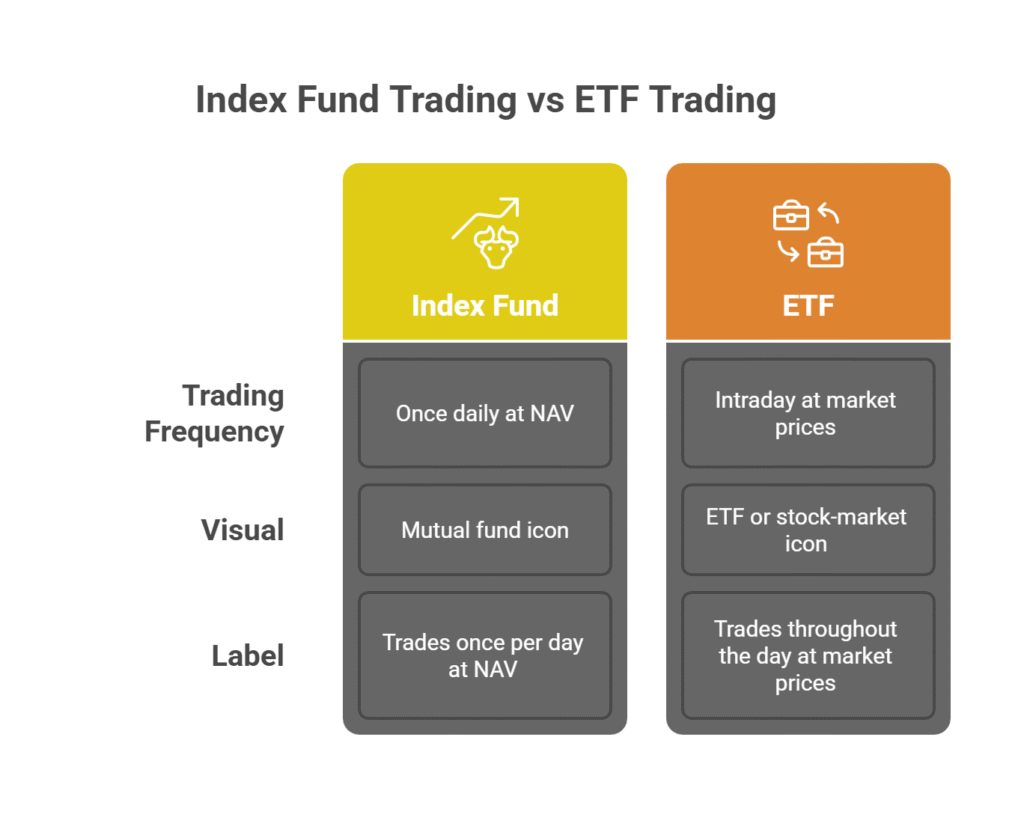

1. Trading Flexibility

The most obvious difference lies in how each investment is traded. Index funds can only be bought or sold once per day, after the market closes, at the fund’s net asset value (NAV). ETFs, on the other hand, trade on exchanges like stocks, allowing you to buy or sell them throughout the trading day.

What This Means for You

- ETFs: Offer flexibility for investors who want to react to market movements or rebalance throughout the day. You can use stop-loss or limit orders and even short-sell ETFs if desired.

- Index Funds: Perfect for investors who prefer a simple, “set it and forget it” approach, without worrying about intraday fluctuations.

For long-term investors, this flexibility may not matter much, but it is worth considering if you like having more control over your trades.

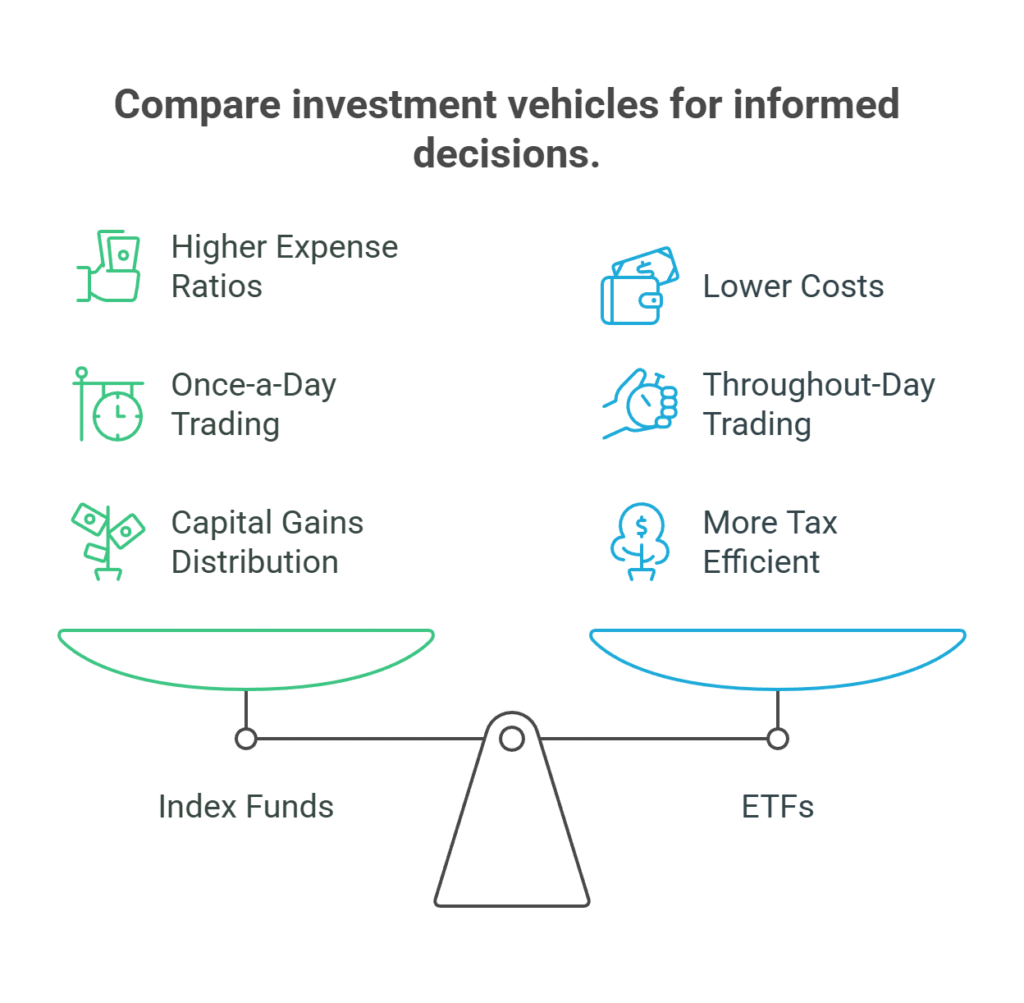

2. Fees and Expense Ratios

Both index funds and ETFs are known for being cost-efficient compared to actively managed funds. However, ETFs typically have slightly lower expense ratios due to their passive, exchange-based structure.

For example, a typical S&P 500 index fund might have an expense ratio of 0.10%, while an ETF tracking the same index might cost 0.03%. That might seem insignificant, but over decades, this difference compounds dramatically. On a $100,000 investment over 30 years, that 0.07% difference could mean thousands of dollars in additional returns.

However, ETFs may involve small brokerage trading fees, depending on your platform, whereas many index funds allow free automatic investments, making them ideal for dollar-cost averaging with small, consistent contributions.

3. Minimum Investment Requirements

Index funds often require a minimum investment, typically between $500 and $3,000 depending on the provider. ETFs, on the other hand, can be purchased for as little as the price of one share, making them far more accessible to beginners.

For instance, if an ETF trades at $120 per share, that is all you need to get started. Many modern brokerages even allow fractional share investing, so you can buy as little as $5 worth of an ETF.

4. Tax Efficiency

ETFs generally have an edge in tax efficiency due to their unique “creation and redemption” process. When large investors (called authorized participants) exchange ETF shares, they do so using in-kind transfers of the underlying assets. This structure helps avoid triggering capital gains taxes for other investors in the fund.

Index funds, on the other hand, may distribute capital gains when the fund manager buys or sells assets, even if you didn’t personally sell your shares. While both are tax-friendly compared to active funds, ETFs tend to win this round.

Performance, Does One Outperform the Other?

Since both track the same underlying indexes, their long-term performance is nearly identical. The main differences arise from expense ratios and tracking errors (minor deviations between the fund’s return and the index it tracks).

Historically, ETFs have shown slightly better performance, often by a fraction of a percent, primarily because of lower costs and reduced capital gains distributions. But this difference is usually minimal in the big picture. For most investors, the choice between an S&P 500 ETF and an S&P 500 index fund will not drastically impact returns.

Example Case Study

Let’s say you invest $10,000 in two funds tracking the S&P 500, one an index fund with a 0.08% expense ratio, the other an ETF with 0.03%. Assuming a 7% average annual return over 30 years:

- Index Fund (0.08% fees): ~$74,000 after 30 years

- ETF (0.03% fees): ~$76,000 after 30 years

The difference, about $2,000, might not sound huge, but that is money staying in your pocket, not lost to fees. The takeaway, lower costs always enhance long-term compounding.

Advantages of Index Funds

- Automatic Investing: You can set up recurring contributions directly from your bank account, perfect for dollar-cost averaging.

- Simplicity: No need to manage trades or worry about timing; your investments happen automatically.

- Great for Retirement Accounts: Many 401(k)s and IRAs make it easy to invest in index funds with minimal maintenance.

Common Drawbacks

- Limited trading flexibility, trades only once daily.

- Minimum investment requirements can be high for beginners.

- Potentially less tax-efficient than ETFs.

Advantages of ETFs

- Real-Time Trading: Buy or sell anytime during market hours.

- Low Expense Ratios: Often cheaper to hold long term.

- High Tax Efficiency: Especially beneficial for taxable brokerage accounts.

- Accessibility: No minimum investment; ideal for small investors.

Potential Drawbacks

- Less convenient for automatic investing (requires manual or scheduled trades).

- Exposure to emotional trading frequent price changes can tempt investors to buy/sell too often.

- Possible small brokerage transaction costs (though many platforms now offer commission-free ETFs).

Which Should You Choose?

Choose Index Funds If:

- You prefer automation through regular, hands-off investing.

- You use a retirement plan like a 401(k) or IRA.

- You’re focused purely on long-term compounding, not daily price swings.

Choose ETFs If:

- You value flexibility and want to trade throughout the day.

- You invest via a brokerage account and want ultra-low fees.

- You care about tax efficiency and plan to hold investments in a taxable account.

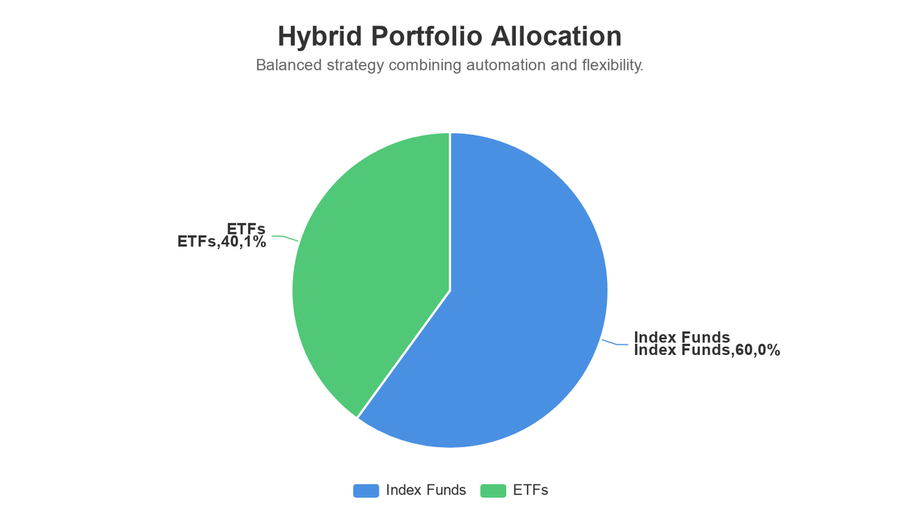

Combining Both Strategies

In reality, many smart investors use both index funds and ETFs in their portfolios. For example:

- Use index funds in retirement accounts (401(k), IRA) for automated contributions.

- Use ETFs in brokerage accounts for greater flexibility and tax efficiency.

This hybrid approach gives you the best of both worlds, consistency and control, without overcomplicating your strategy.

Common Mistakes to Avoid

- Overtrading ETFs: Treat ETFs as long-term investments, not day-trading tools.

- Ignoring Fees: Even small differences in expense ratios add up.

- Not Considering Taxes: ETFs are generally better for taxable accounts; index funds suit tax-advantaged ones.

- Neglecting Diversification: Do not just pick one fund, diversify across asset classes and regions.

Frequently Asked Questions

1. Can I lose money with ETFs or index funds?

Yes, both follow market performance, meaning if the overall market declines, so will your investment. However, they are far less risky than individual stocks and tend to recover over time, especially with a long-term horizon.

2. Are ETFs safer than index funds?

Both are equally safe when tracking the same index. Safety depends more on diversification and holding period than on the fund type itself.

3. Can I automatically invest in ETFs?

Some brokers now allow automated ETF investments, but traditionally this was easier with index funds. If automation is your priority, stick with index funds or use recurring ETF buys where available.

4. Which has better returns, ETFs or index funds?

Returns are nearly identical since both track the same indexes. Any difference comes from small fee variations or tracking errors.

5. Can I hold both ETFs and index funds in my portfolio?

Absolutely. Many investors use both strategically — index funds for simplicity and ETFs for tax and trading flexibility.

Final Thoughts

When comparing index funds vs ETFs, the truth is simple. Both are outstanding vehicles for long-term investors. They provide easy diversification, low costs, and passive exposure to the world’s biggest markets, all essential elements for sustainable wealth building.

If you value simplicity and automation, index funds are your best friend. If you prefer flexibility, control, and slightly better tax efficiency, ETFs may be the smarter choice. Ultimately, the best option depends on your investment habits, goals, and tax situation.

Pro Tip, Do not overthink it. Pick one, start investing, and stay consistent. The real key to long-term success is not the fund you choose, it is your discipline to stay invested and let compounding do the heavy lifting.