Your credit card score plays a massive role in whether you’re approved when applying online. Whether you’re chasing cashback cards, travel perks, or simply trying to build credit, your score determines your approval odds, credit limit, and interest rate. Many people apply without fully understanding what banks are looking for, then wonder why they were denied.

In this complete guide, you’ll learn how lenders evaluate you during credit card online approval, what the minimum credit score for online credit card approval typically is, how to boost your score before applying, and how that same score affects your ability to qualify for loans. We’ll also provide practical steps to help you succeed, even if your score isn’t perfect yet.

Understanding Your Credit Card Score

Before applying for a card online, it’s important to understand what your credit card score actually is.

Most lenders use either FICO or VantageScore models, which evaluate your creditworthiness on a scale from 300 to 850. The higher your score, the better your approval odds and the lower your interest rate. This three-digit number is based on information in your credit file from agencies like Experian, Equifax, and TransUnion.

Score Ranges

- Excellent: 800–850

- Very Good: 740–799

- Good: 670–739

- Fair: 580–669

- Poor: 300–579

Your credit card score influences everything from whether you’re approved to how much interest you pay.

Even a 40–60 point improvement can help you move into a better category and unlock better offers.

What Determines Your Score?

Here’s a breakdown of the factors that shape your credit score:

- Payment history (35%): On-time payments are crucial.

- Utilization (30%): Keep credit balances low compared to your limit.

- Credit age (15%): Older accounts show financial maturity.

- Credit mix (10%): A variety of accounts supports higher scores.

- New credit (10%): Too many applications can hurt your score.

To dig deeper into how credit scoring works, see:

https://investwisetoday.com/experian-credit-score-free-report-guide/

How Your Credit Card Score Impacts Online Approval

When you apply for a credit card online, the issuer typically runs a hard inquiry on your credit report.

This inquiry gives them access to your credit card score and full profile.

They use this information to determine whether you’re a high or low risk.

Higher scores signal that you’re likely to pay your bills on time. Lower scores suggest risk, so issuers may deny your application or offer less favorable terms.

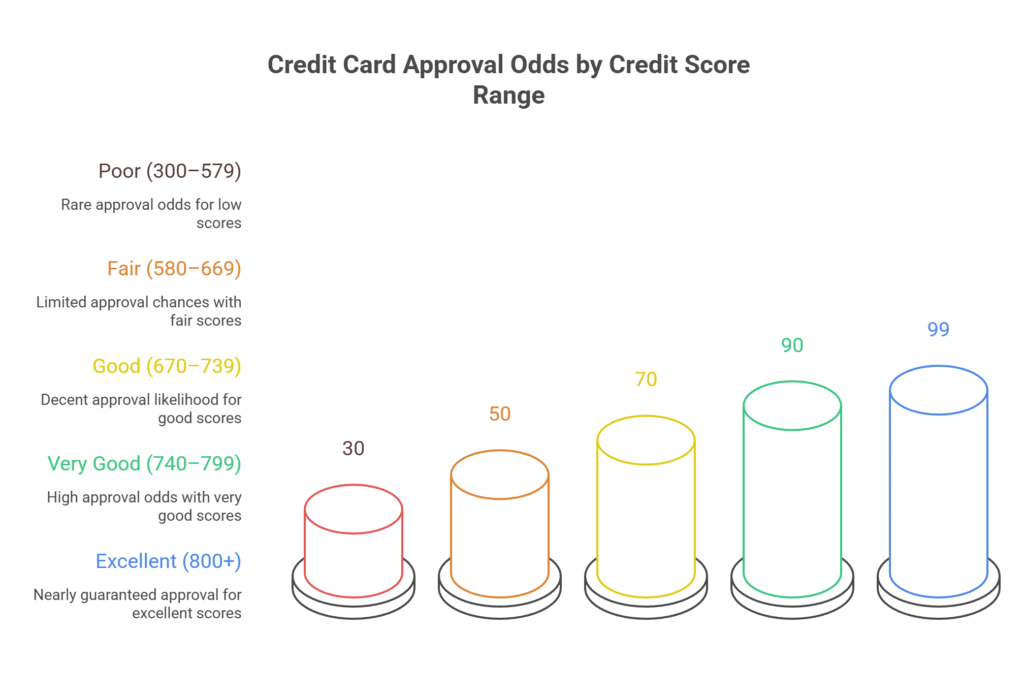

Approval Odds by Score Range

Below is a typical breakdown of how score ranges affect credit card online approval:

- Excellent (800+): Nearly guaranteed approval for top cards.

- Very Good (740–799): High approval odds; strong rewards.

- Good (670–739): Decent approval odds; may get mainstream cards.

- Fair (580–669): Limited options; often requires secured cards.

- Poor (300–579): Rare approval; consider credit rebuilding tools.

Every issuer has different internal criteria, but the credit score is often the biggest piece of the puzzle.

Other Factors Lenders Consider

While your credit card score is important, lenders also consider:

- Your income

- Your debt-to-income ratio

- Your credit history length

- Recent credit applications

So, even if you have a great score, if your income doesn’t support a large credit line or you’ve applied for many cards recently, you might be denied.

Minimum Credit Score for Online Credit Card Approval

There’s no universal “minimum” score for approval, but there are general guidelines.

Your credit card score determines the tier of cards available to you.

Typical Minimum Score Requirements

- Excellent cards: 740+

- Mid-tier rewards cards: 680–739

- Starter cards: 600–679

- Secured cards: Below 600

If your score is below 580, approval becomes very unlikely without a secured card.

Quick Example

Emma has a score of 725. She applies online for a travel rewards card. Because she has strong credit history and a moderate income, she’s approved.

Jack has a 610 score. He applies for the same card and is denied. He is approved for a secured card and later upgrades.

How to Improve Your Credit Score Before Applying

If your score falls below the typical requirements for the card you want, don’t panic.

There are several ways to improve your score quickly sometimes within 30–60 days.

1. Pay Down Credit Card Balances

Your utilization rate is the amount of credit you’re using compared to your limit has a major impact.

Aim to keep utilization under 30%, ideally under 10%.

If your balance is $900 on a $1,000 limit, your utilization is 90%, a big red flag to lenders.

2. Correct Inaccuracies on Your Report

Errors happen. An incorrect late payment or fraudulent account can lower your score.

Dispute any issues with the credit bureau to have them removed.

Learn how to do this here: [LINK: Free Credit Score and Report — What You Need to Know]

3. Bring Delinquent Accounts Current

Late payments have a large impact. Catching up even if you can’t fix old late marks still improves your score over time.

4. Limit New Applications

Every application triggers a hard inquiry. Multiple inquiries in a short period can lower your score and signal desperation.

5. Become an Authorized User

If a family member has a strong credit history, being added to their account can improve your score significantly.

Mini Case Study

Alex had a 650 score and struggled to get approved. He paid down two credit cards below 30% utilization, corrected a reporting error, and was added as an authorized user on a parent’s account.

Within 60 days, his score rose to 695 enough to qualify for a mid-tier cashback card.

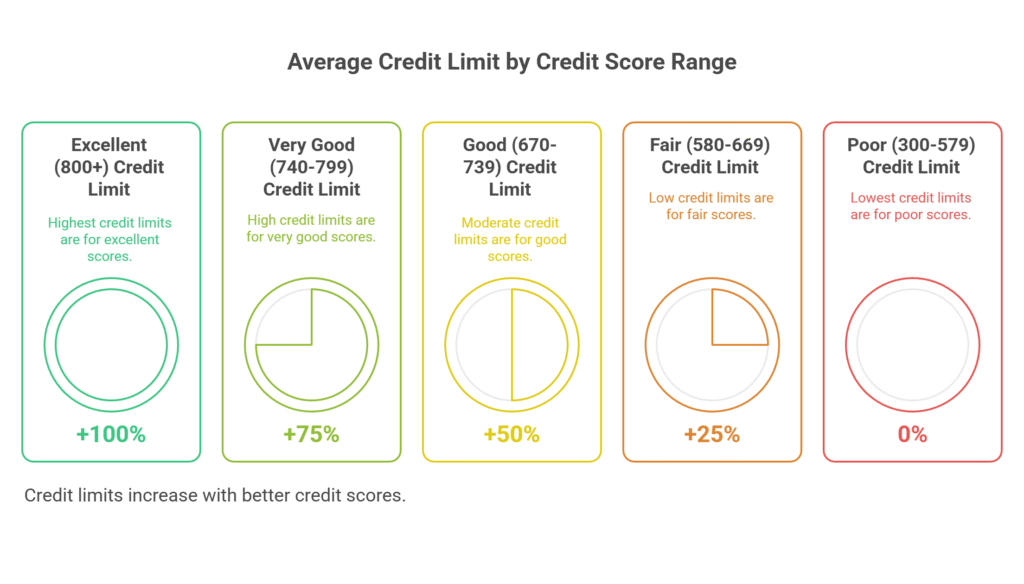

How Your Credit Card Score Affects Your Credit Limit & APR

Most people think approval is the end goal but your credit card score also determines

how much credit you receive and the interest rate (APR) you pay.

Even if you are approved, a lower score usually means:

- Lower starting credit limit

- Higher interest rates

- Fewer benefits/rewards

For example, someone with a 780 score could be approved for a $12,000 limit with a 19% APR, while someone with a 650 score might get a $1,000 limit with a 30% APR.

That difference affects your buying power and how much interest you pay over time.

Why Credit Limits Matter

Your credit limit affects your utilization ratio.

If you have a low limit and your balance runs high, your score can drop quickly.

Example:

If you spend $800 on a $1,000 limit card → 80% utilization.

Negative impact.

If you spend $800 on a $5,000 limit card → 16% utilization.

Positive impact.

This is why improving your credit score before applying can help you secure a higher credit limit,

which in turn keeps your utilization lower and can help improve your score further.

How Credit Card Score Influences Loan Approval

The same factors lenders use to evaluate your credit card score also influence your

ability to get approved for other loans especially personal loans, auto loans, and mortgages. Understanding how your credit score affects these decisions helps you plan smarter for long-term goals.

Minimum Credit Score for Loan Types

- Personal loan: ~610–640+ (minimum), 700+ preferred

- Auto loan: ~600+ (minimum), 660+ preferred

- Mortgage: 620+ minimum (conventional), 740+ preferred

So, even if your goal isn’t just a new card, raising your score increases your approval odds across all credit types.

Personal Loan Example

Two borrowers apply for a personal loan:

- Borrower A: Score = 760

- Borrower B: Score = 640

Borrower A gets a 7% APR, while Borrower B gets a 19% APR.

Over a 3-year term, that difference can cost Borrower B thousands more.

This shows how your credit card score plays into long-term financial health beyond cards alone.

How to Prepare for a Credit Card Online Approval

Before applying for a card online, it’s important to prepare so you don’t waste hard inquiries or face unexpected denials. Follow this simple 5-step checklist to increase your odds.

1. Check Your Credit Score First

Always verify your score before applying. A soft-pull tool gives you an up-to-date number without hurting your score.

Start here:

[LINK: Free Credit Score and Report — What You Need to Know]

2. Review Your Credit Report

Check for errors, fraud, or outdated data. Fixing issues before applying can boost your odds immediately.

3. Compare Cards Based on Score Requirements

Don’t waste inquiries look for cards designed for your credit tier.

4. Reduce Utilization

Pay down balances to under 30% (preferably under 10%). This can boost your score fast and improve approval odds.

5. Avoid Multiple Applications

Every online application adds a hard inquiry. Too many in a short period signals risk to lenders.

Why Timing Matters When You Apply

Sometimes approval isn’t just about your score it’s about timing. Strategic timing can improve your odds more than you think.

1. After a Balance Paydown

Card issuers report balances monthly. If you pay down debt before your statement closes, your utilization drops and your score may rise before you apply.

2. After Removing Errors

If you dispute a reporting error, wait until the correction appears before applying.

3. After Age Increases

If you recently opened accounts, waiting 3–6 months adds helpful account age and distance from recent inquiries.

4. After Becoming an Authorized User

Give reporting a month or two to show up before applying.

Try Secured Cards if You Have Bad Credit

If your credit card score is too low for traditional approval, a secured credit card may be your fastest way to rebuild credit.

How Secured Cards Work

You place a refundable security deposit (e.g., $200–$500). The issuer provides a card with a matching limit. You use it like any card responsibly and they report activity.

Why They Help

- Easier approval

- Builds credit history

- Graduates to unsecured card in 6–12 months

After responsible use, you may upgrade and get your deposit back.

Smart Ways to Boost Your Credit Score Fast

If you’re planning to apply soon, these strategies can help you increase your score quickly sometimes within 30–60 days.

1. Pay Before the Statement Date

This reduces the balance reported, lowering utilization.

2. Ask for a Credit Limit Increase

More available credit = lower utilization. But ask only if your account is in good standing.

3. Keep Old Cards Open

Closing cards lowers your average account age and can raise utilization.

4. Dispute Errors

Incorrect late payments or balances can tank your score. Fixing them can help instantly.

5. Add Positive Credit History

If you’re new to credit, become an authorized user to gain age and history.

Case Study: From Denial to Approval

Sara applied online for a cashback card with a credit card score of 640.

She was denied because of high utilization and a short credit history.

She followed a 60-day plan:

- Paid down utilization to 20%

- Corrected a reporting error

- Was added as an authorized user

Her score rose to 695. She reapplied this time with approval and a $4,500 limit.

Common Mistakes When Applying for Online Credit Cards

- Applying without checking your score

- Multiple applications in a short time

- Ignoring utilization rate

- Closing old accounts before applying

- Applying for premium cards with weak credit

Avoiding these simple mistakes can dramatically increase your approval chances.

Frequently Asked Questions

1) What is a good credit card score?

A good score is typically 670+, though 740+ opens the door to premium cards.

2) Does applying online hurt my score?

Yes! Every online application triggers a hard inquiry, which can temporarily lower your score.

3) What is the minimum credit score for online credit card approval?

Typically around 620–650 for entry-level cards, but premium cards may require 740+.

4) Can I get approved with poor credit?

Yes! Secured cards and rebuilding products are available.

5) Does my credit score affect my credit limit?

Yes! Higher scores typically receive higher limits and lower APRs.

Takeaways

Your credit card score is more than just a number it’s a key that unlocks credit card online approval,

better interest rates, higher limits, and access to premium financial products.

Whether you’re aiming for your first card or leveling up to elite travel rewards, understanding how your score is evaluated and improving it before you apply can dramatically boost your odds of approval.

Remember: there is no universal minimum credit score for online credit card approval, but the higher your score, the better your offers.

Likewise, your credit card score plays a major role when securing loans, especially personal loans, auto loans, and mortgages.

A stronger score means more borrowing power and lower costs over time.

If your score needs improvement, don’t panic. With a focused plan reducing utilization, fixing errors, becoming an authorized user, and spacing applications you can see real progress within 30–90 days.

Use this guide as your roadmap, and apply responsibly.

✅ Next steps:

- Check your credit score before applying

- Review your credit report for errors

- Compare cards suited to your score range

- Raise your score using the strategies above