A free credit score and report gives you a complete picture of your financial health. Unlike bank balances or income alone, your credit profile determines whether you can rent an apartment, finance a car, or qualify for a low-interest credit card. Fortunately, checking your credit score and credit report has never been easier or more important.

This guide explains why your score matters, how to get your free credit score report, what “credit score sites free” really means, and how to read and use your report to improve your financial life.

Why Your Credit Score and Report Matter

People often focus on income or job stability when thinking about financial readiness. But lenders, landlords, utilities, and sometimes employers rely on your credit profile to evaluate risk. Your score is essentially a grade that measures how reliably you repay your debts. Meanwhile, your credit report shows the story behind that score, your accounts, balances, payment history, and any negative items. Together, a free credit score and report gives you the information you need to manage, repair, or optimize your financial life.

How Credit Scores Influence Your Daily Life

Your credit score affects far more than loans. From approving credit cards to setting deposit requirements, it determines how expensive or affordable life becomes.

- Loan Approvals: Higher scores lead to easier approvals and better terms.

- Interest Rates: Good credit = lower interest; bad credit = higher costs.

- Insurance Premiums: Some insurers price based on credit behavior.

- Apartment Rentals: Landlords often require background and credit checks.

- Utility Deposits: Low scores may increase required deposits.

Even small changes in your credit score can create major financial advantages.

For instance, improving your score from “Fair” to “Good” could reduce a mortgage interest rate by 1% or more.

That difference could save tens of thousands over the course of a 30-year mortgage.

That is the power of knowing and managing your score.

Why Checking Your Credit Doesn’t Hurt Your Score

A common fear is that checking your score lowers it.

This is only true when a bank performs a “hard inquiry”, usually when you apply for new credit.

However, reviewing your own free credit score and report is a soft inquiry and will never hurt your score.

Checking regularly is one of the smartest habits you can build.

The Difference Between a Free Credit Score and a Free Credit Report

One of the biggest sources of confusion is the difference between a free credit score and a free credit report.

They are related, but not the same and you need both to make informed decisions.

What Is a Free Credit Score?

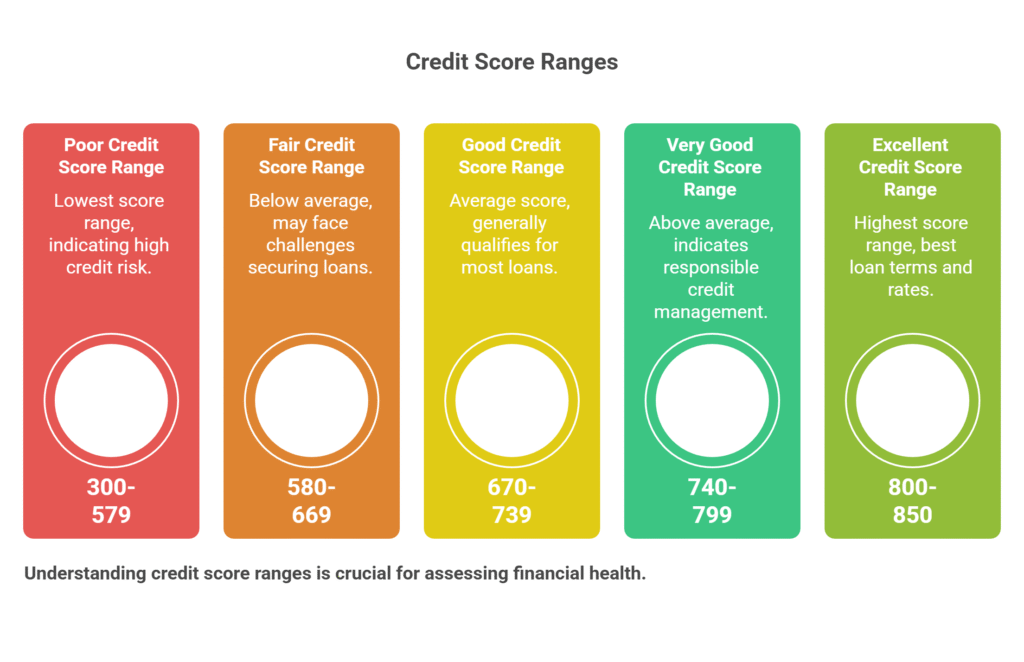

Your credit score is a three-digit number, often based on FICO or VantageScore, that summarizes your creditworthiness. Many consumers see score ranges like:

- Excellent: 800–850

- Very Good: 740–799

- Good: 670–739

- Fair: 580–669

- Poor: 300–579

Scores are influenced by factors such as:

- Payment history

- Credit utilization

- Length of credit history

- Types of credit used

- New credit/inquiries

Your score tells lenders at a glance how risky you are.

It’s helpful for quick checks and long-term progress tracking.

What Is a Free Credit Report?

Your credit report is a detailed record of your financial history.

It includes:

- Open and closed accounts

- Account balances and limits

- Payment history

- Collections

- Public records

- Hard inquiries

While your score is just a summary number, your report tells the full story.

If there’s a drop in your score, the report helps you identify why.

Why You Need Both

Tracking just the score is like monitoring your weight without looking at your diet or habits.

The score tells you where you are; the report tells you what’s driving the results.

How to Get a Free Credit Score and Report

There are multiple ways to access your free credit score and report. Some platforms offer only scores. Others provide full reports.

Some provide both, and many are legitimately free. Be cautious of trials that require credit card details unless you are comfortable managing cancellations.

The Safest Way to Get a Free Credit Report

In the U.S., the official source for full bureau reports is:

https://www.annualcreditreport.com

You can access one report from each bureau (Experian, TransUnion, Equifax) yearly.

In some countries, consumers can request reports through their national credit authorities.

Free Credit Score Options

To get a free score, many consumers use:

- Experian’s online portal often includes score + insights

- Major bank dashboards

- Credit score sites free tools

- Personal finance apps and platforms

Choose reputable providers that specify “soft inquiry” this ensures your score won’t be affected.

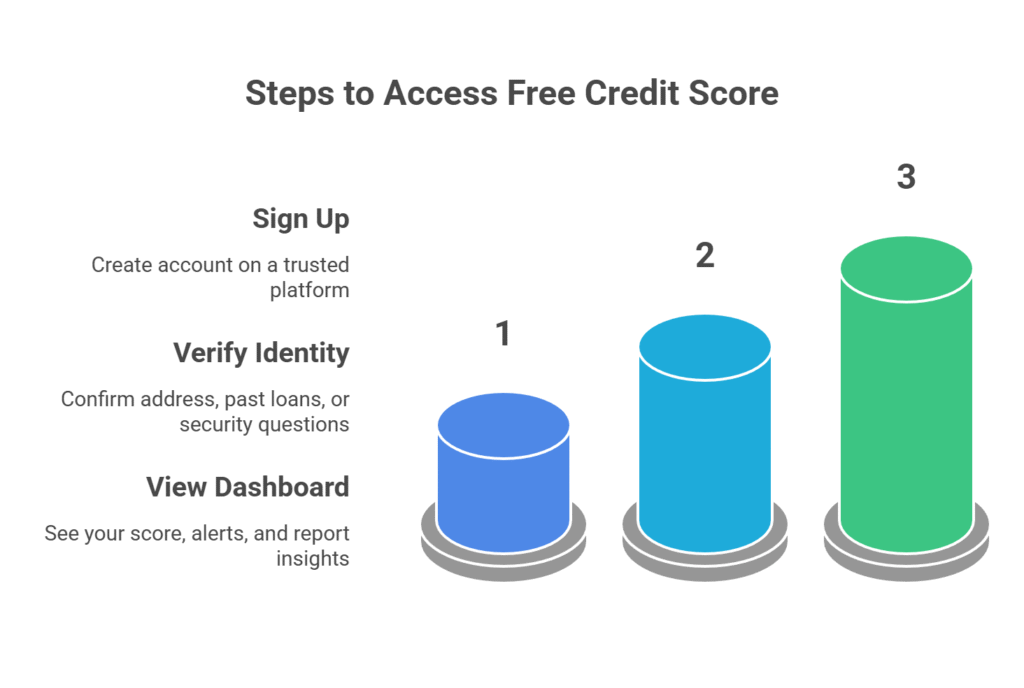

Step-by-Step Guide to Accessing Your Free Score

- Sign up on a trusted platform.

- Verify identity (address, past loans, etc.).

- Access your free credit score report dashboard.

- Review score, alerts, and changes over time.

- Download your full report if available.

Pro Tip: Set up alerts, many platforms notify you of suspicious activity, new accounts, or balance spikes.

Not sure where to begin? Start here:

https://investwisetoday.com/experian-credit-score-free-report-guide/

Comparing the Best Credit Score Sites That Are Free

Not all “free credit score” websites are equal. Some use aggressive upsells; others offer limited data. Below is a comparison of popular tools offering a free credit score and report or either individually.

Leading Free Sources

| Service | Free Score? | Free Report? | Bureau Source | Notes |

|---|---|---|---|---|

| Experian Portal | Yes | Yes | Experian | Highly trusted; clear explanations. |

| AnnualCreditReport | No | Yes | Experian, Equifax, TransUnion | Best for full official reports. |

| Bank Apps | Yes | No | Varies | Convenient; soft pulls only. |

| General score sites | Yes | Sometimes | Varies | Mixed quality—use caution. |

These platforms are useful starting points.

However, for complete visibility, always pair your free score with a full report from one of the three major bureaus.

How to Read Your Credit Report for Free

Once you get your free credit score and report, the next step is analysis.

Understanding what you’re looking at helps you track progress, fix errors, and spot identity theft early.

Key Sections to Review

Your report typically includes:

- Personal Information: Name, SSN, address history

- Accounts: Loans + credit cards

- Payment History: On-time or late payments

- Balances & Limits: Used credit vs available

- Inquiries: Hard vs soft inquiries

- Collections: If applicable

Make sure all entries are correct.

Errors, like accounts you do not recognize, can be signs of identity theft or misreporting.

Identifying Red Flags

- Unknown accounts

- Incorrect late payments

- Balances that don’t match statements

- Repeated hard inquiries

If you spot inaccuracies, file a dispute with the relevant bureau.

Correcting errors can raise your score quickly.

How to Improve Your Score After Reviewing Your Report

Getting your free credit score and report is step one using it to improve your rating is step two.

Here’s a proven process to build (or rebuild) credit in 30–90 days.

Step-by-Step Strategy

- Fix errors quickly: Submit disputes with evidence.

- Pay on time: Even one late can hurt.

- Lower utilization: Keep use <30%—preferably <10%.

- Pay before statement date: Lowers reported balance.

- Request a limit increase: Helps utilization.

- Minimize applications: Avoid unnecessary hard pulls.

- Keep old accounts open: Boosts account age.

Mini Case Study

A borrower with a 620 score reduced utilization from 70% to 25%, disputed an incorrect late payment, and added a secured card. Within 90 days, the score reached 690—enough to qualify for a lower-rate consolidation loan.

Savings: several hundred euros per year.

Common Mistakes to Avoid

- Confusing “score” with “report”

- Paying for overpriced credit monitoring

- Checking only one bureau’s report

- Ignoring small collections

- Closing old credit cards unnecessarily

Frequently Asked Questions

1) Does checking my credit score lower it?

No, soft inquiries do not affect your score. Only hard pulls (from applications) can temporarily reduce it.

2) Which credit score sites are free?

Experian, many bank dashboards, and other personal finance platforms offer credit score sites free

tools with no impact on your rating.

3) How often should I check my credit?

Monthly is ideal. Score changes as lenders report data.

Reports should be reviewed at least once per year.

4) Can I get all three reports for free?

Yes. In the U.S., you can access annual reports from Experian, Equifax, and TransUnion via

https://www.annualcreditreport.com.

5) Should I pay for a score?

Usually no. You can obtain both a free credit score report and a free full report through legitimate channels.

Conclusion. Take Control With Your Free Credit Score and Report

Understanding your free credit score and report is the foundation of financial wellness.

It helps you catch mistakes, protect against fraud, qualify for better financial products,

and improve your long-term economic outlook.

The tools and steps in this guide empower you to take control today.

✅ Next steps:

- Check your free Experian credit report

- Review your score monthly

- Dispute any errors

- Follow a 30-90 day improvement plan

Get started now.

Check your free Experian credit report today.