Building an emergency fund is one of the most important steps toward achieving financial security. Many beginners struggle to grow their savings effectively due to distractions, lifestyle expenses, or lack of clear planning. This guide provides actionable strategies to maximize your emergency fund, stay consistent, and protect yourself against unexpected expenses. Whether you’re new to budgeting or looking for advanced strategies, these tips will help you reach your financial safety goals efficiently.

Why an Emergency Fund Matters

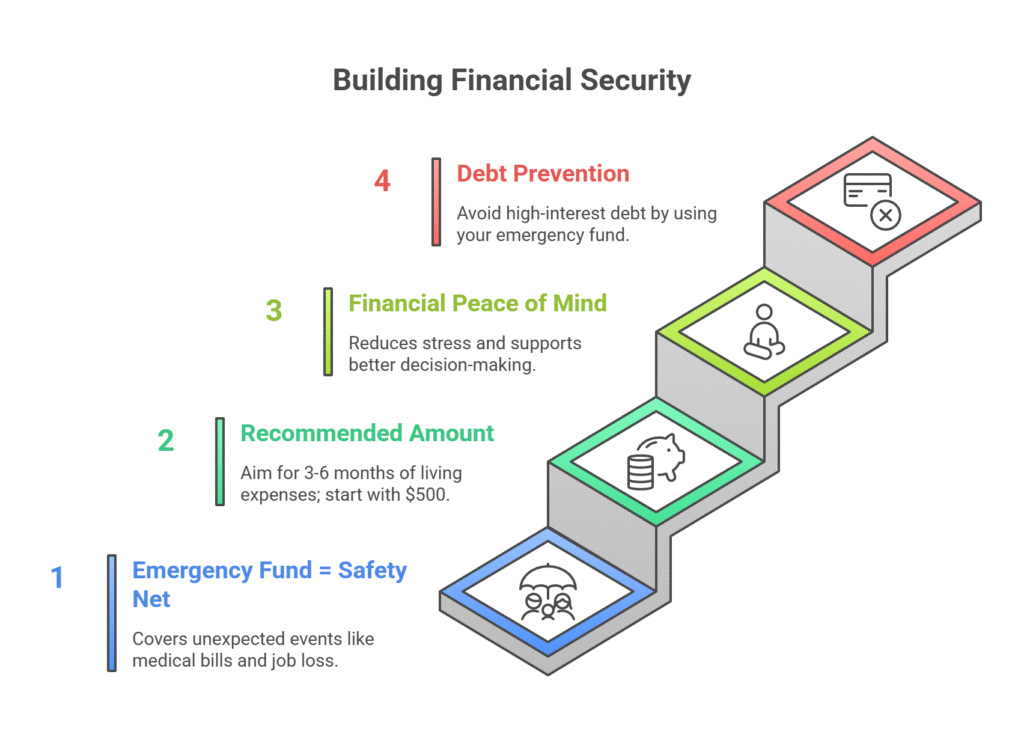

An emergency fund acts as a financial safety net, helping you avoid debt when unforeseen events occur. Life is unpredictable medical emergencies, car repairs, or sudden job loss can happen at any time. Experts recommend saving at least three to six months’ worth of living expenses. Building this fund not only improves financial resilience but also provides peace of mind, reduces stress, and ensures you can make decisions without panic.

Financial Peace of Mind

Knowing you have money set aside reduces financial anxiety. Beginners often start small, with goals as low as $500, and gradually increase contributions. Even a modest emergency fund allows you to handle minor expenses without turning to high-interest debt. For additional guidance, check our beginner-friendly budgeting guide.

Preventing High-Interest Debt

Without an emergency fund, people often rely on credit cards or personal loans during unexpected events, leading to high-interest debt that is difficult to manage. By prioritizing your fund, you avoid this trap and gain control over your finances. A structured fund ensures you’re prepared and can avoid compounding interest charges from debt accumulation.

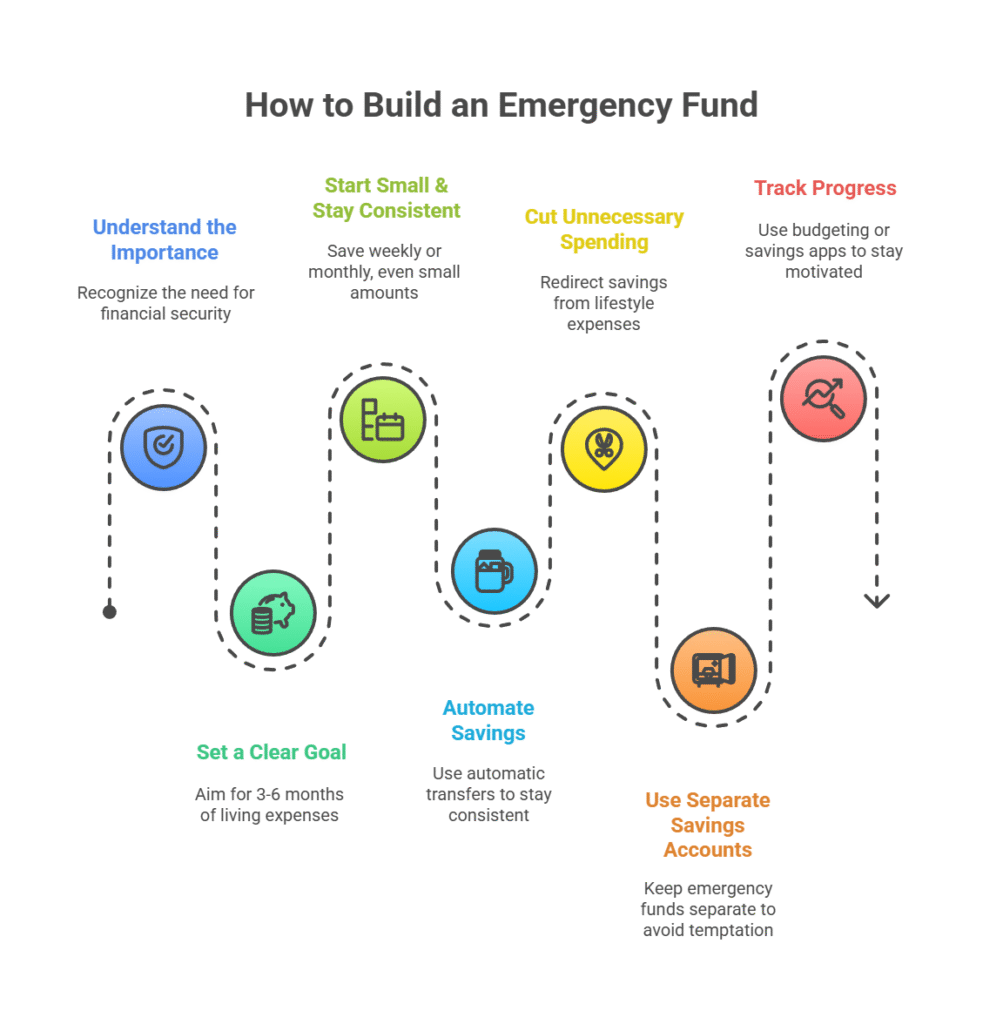

Step-by-Step Strategies to Grow Your Emergency Fund

Growing your emergency fund requires a mix of planning, discipline, and smart financial strategies. Below are actionable steps that can guide beginners and experienced savers alike.

1. Set Clear, Realistic Goals

Define exactly how much you want to save and by when. Break your ultimate target into smaller milestones, such as saving $1,000 before tackling three months of expenses. Goal-setting increases motivation and provides measurable progress checkpoints.

- Calculate your monthly living expenses accurately, including rent, utilities, groceries, insurance, and essential spending.

- Set a target amount for short-term milestones (e.g., $500, $1,000, $2,500).

- Use visual progress trackers or charts to maintain motivation.

Small, incremental targets help you maintain momentum without feeling overwhelmed. Celebrating small wins reinforces positive savings behavior.

2. Automate Your Savings

Automation is crucial for consistency. Schedule recurring transfers to a dedicated savings account even a small amount like $50 per month accumulates significantly over time. Automation reduces the temptation to spend and ensures you consistently contribute without relying on willpower alone.

- Use your bank’s online banking system or mobile app to set up automatic transfers.

- Consider apps or budgeting platforms that allow “round-up” savings from daily purchases.

- Monitor contributions periodically to adjust for income changes or unexpected expenses.

Automating savings helps you make steady progress toward your goals and removes psychological barriers associated with manual deposits.

3. Cut Unnecessary Expenses

Review your monthly budget and identify non-essential spending that can be redirected toward your emergency fund. Even small savings add up over time, accelerating your progress.

- Reduce or eliminate streaming subscriptions you rarely use.

- Prepare meals at home instead of dining out frequently.

- Switch to more affordable alternatives for routine expenses like coffee, phone plans, or utilities.

- Leverage cashback and reward programs to supplement your fund.

For example, cutting $25 weekly from discretionary spending frees up $100 per month, or $1,200 annually enough to reach initial emergency fund milestones faster.

4. Increase Your Income

Boosting your savings rate can dramatically accelerate fund growth. Options include side hustles, freelance work, or monetizing hobbies. Extra income directly applied to your emergency fund reduces time needed to reach your goals.

- Freelancing or consulting in your skill area https://www.upwork.com/

- Part-time work or gig economy jobs

- Selling unused items or crafts online.

- Monetizing small talents such as tutoring, graphic design, or writing

Extra income allows you to contribute more aggressively while maintaining your regular budget. Even modest additional earnings can shorten the timeline to a fully funded emergency reserve.

5. Use Cash Windfalls Wisely

Windfalls, such as tax refunds, work bonuses, or monetary gifts, provide an opportunity to accelerate your emergency fund. Allocate a portion or all of these unexpected funds directly to your savings to create a habit of prioritizing financial security.

- Deposit 50–100% of bonuses into your emergency fund.

- Apply at least a portion of tax refunds for consistent fund growth.

- Track progress and adjust contributions to maintain your target timeline.

By applying windfalls strategically, you can reach emergency fund goals faster without significantly altering your monthly budget.

Advanced Tips for Faster Growth

Once your basic emergency fund framework is established, these advanced strategies can further maximize growth and ensure your savings maintain value.

High-Yield Savings Accounts

Parking your fund in a high-yield savings account allows it to earn interest passively. Look for accounts with competitive rates, no monthly fees, and FDIC insurance. Even modest contributions gain extra value thanks to compound interest.

- Compare multiple banks to find the best rates https://www.bankrate.com/banking/savings/rates/

- Set up automatic transfers to the high-yield account

- Monitor interest accrual and reinvest earnings

Cash-Back and Rewards Programs

Redirecting rewards from cashback cards or apps into your emergency fund creates a passive growth stream. While incremental, these small additions compound over time and contribute to overall fund growth.

- Use cashback credit cards responsibly.

- Convert rewards points directly into savings or cash deposits

- Track reward accumulation and transfer periodically

Common Mistakes to Avoid

Withdrawing for Non-Emergencies

Using your emergency fund for planned purchases undermines its purpose. Keep it strictly for unforeseen events to maintain its effectiveness and security.

Setting Unrealistic Goals

Overambitious targets can lead to frustration and abandonment. Break goals into manageable steps, and increase contributions gradually as your income and financial discipline improve.

Ignoring Inflation

Inflation reduces the real value of your savings over time. Periodically reassess your target emergency fund and adjust contributions to maintain adequate purchasing power. Consider incorporating slightly higher savings targets to offset inflation impacts.

![]()

Frequently Asked Questions

1) How much should a beginner save for an emergency fund?

Start with a goal of $500–$1,000, then gradually work up to covering three to six months of essential living expenses. Begin small, build confidence, and scale up contributions over time.

2) Can I keep my emergency fund in a checking account?

While checking accounts offer accessibility, a high-yield savings account is preferable. It provides interest growth while maintaining liquidity for emergencies.

3) How fast can I realistically build an emergency fund?

Consistent savings combined with small lifestyle adjustments allow many beginners to establish a basic emergency fund in 6–12 months. Aggressive strategies such as extra income allocation or windfall contributions can reduce this timeline significantly.

4) Should I combine automation with manual contributions?

Yes, automation ensures consistency, while manual contributions allow flexibility during windfalls or extra earnings periods. Combining both maximizes fund growth while maintaining discipline.

5) Is it okay to invest a portion of my emergency fund?

Generally, emergency funds should remain in liquid, low-risk accounts. Investing in volatile assets could compromise accessibility during emergencies. However, some portion